The ban on residential property LRBAs landed in 2026 and shut the door on the strategy most SMSF trustees had in mind when they googled “borrow inside my super”. No more using a limited recourse borrowing arrangement to buy a house, unit, or apartment inside your fund. The amended legislation is clear and it is not coming back (with the current Government anyway).

There is, however, one property strategy where LRBA borrowing remains completely intact — and it is arguably more powerful than anything residential ever was. Your SMSF can still borrow to buy commercial property, provided that property qualifies as business real property under s.66 of the Superannuation Industry (Supervision) Act 1993 (SIS Act). An SMSF commercial property loan structured as an LRBA is legal, lender-ready, and — if you are a business owner — one of the smartest wealth-building moves available to you.

This guide covers everything: the legal definition of business real property, how the loan structure works, current lender rates, the leaseback strategy, and the compliance traps that catch people out. If you are serious about buying commercial premises inside your super fund, start here.

The key borrowing strategy that survived the 2026 LRBA ban

The 2026 LRBA ban prohibits SMSFs from entering into new limited recourse borrowing arrangements where the asset being acquired is residential property. The ban applies to new arrangements entered into (contracts signed) after the commencement date (expected to be 10 August 2026) — existing residential LRBAs are not unwound, but no new ones can be established. It is a significant change and it affects the majority of SMSF property investors who were looking at the residential market.

What many trustees do not realise is that the same legislation that introduced the ban also explicitly preserved LRBAs for a specific class of property. The new s.67A(2)(c) of the SIS Act carves out LRBAs where the property is business real property as defined in s.66. That preservation is deliberate — business real property LRBAs serve a legitimate purpose (small business owners funding their own premises through super) and the legislature chose to keep them.

The critical term here is “business real property.” It is a defined legal concept under s.66 of the SIS Act, and it does not mean the same thing as “commercial property” or “non-residential property” or “commercially zoned land.” Understanding exactly what the definition covers — and what it excludes — is the entire game.

What is ‘business real property’? The s.66 SIS Act definition

The definition sits in s.66(5) of the SIS Act, and the ATO’s authoritative interpretation is found in SMSFR 2009/1 — the ATO’s self-managed superannuation fund ruling on business real property. If you are going to hold commercial property in your SMSF, you need to understand this ruling.

The verbatim definition from para 4 of SMSFR 2009/1 reads:

“business real property, in relation to an entity, means:

(a) any freehold or leasehold interest of the entity in real property; or

(b) any interest of the entity in Crown land, other than a leasehold interest, being an interest that is capable of assignment or transfer; or

(c) if another class of interest in relation to real property is prescribed by the regulations for the purposes of this paragraph — any interest belonging to that class that is held by the entity;

where the real property is used wholly and exclusively in one or more businesses (whether carried on by the entity or not), but does not include any interest held in the capacity of beneficiary of a trust estate.”

Para 5 of SMSFR 2009/1 breaks this down into two conditions that must both be satisfied:

- Eligible interest: The entity (your SMSF, or the party from whom it is acquiring the property) must hold an eligible interest in real property — freehold, leasehold, or Crown land capable of assignment or transfer.

- Business use test: The underlying land must be used wholly and exclusively in one or more businesses.

Both conditions must be satisfied. An eligible interest alone is not enough. Meeting both conditions is what turns an ordinary piece of real property into business real property.

Eligible interests — freehold, leasehold and Crown land

Most commercial property transactions involve freehold — outright ownership of the land and the building. That clearly qualifies as an eligible interest (SMSFR 2009/1, paras 9–19).

A leasehold interest also qualifies. If your SMSF holds a long-term lease over land (rather than owning it outright), that can still be business real property provided the business use test is satisfied. Crown land interests capable of assignment or transfer are also included — this matters for farming and rural properties where the title is held under a Crown lease.

What does not qualify is an interest held as a beneficiary of a trust estate. The definition explicitly excludes that. This is relevant if someone tries to use a unit trust structure and argues the SMSF’s unit holding is business real property — it is not.

The business use test — “wholly and exclusively”

This is the test that matters most in practice. Para 20 of SMSFR 2009/1 states it plainly: the real property must be used wholly and exclusively in one or more businesses. Both words carry weight.

Para 26 deals with “wholly”: the land must be used entirely in one or more businesses. Partial business use is not sufficient. If part of the land is used for business and part for something else — storage, personal use, residential — the test fails (at least for that part).

Para 27 deals with “exclusively”: the land must be used only for business purposes. Personal or private use fails the test, even if it is incidental or minor.

Para 23 contains a critical liberating rule: the business does not have to be carried on by the entity holding the property. So your SMSF can hold a property that is used wholly and exclusively in a business carried on by someone else — including a related party like your own company. This is what makes the leaseback strategy work. And of course and unrelated business can also lease the property.

The test is about the use of the land, not who is conducting the business. As long as the land is used wholly and exclusively in a business, the property qualifies — regardless of the relationship between the property holder and the business operator.

What qualifies as business real property (with ATO approved examples from

SMSFR 2009/1)

The ruling provides clear examples of property that satisfies the business use test. These are not edge cases — they represent the core of what the definition is designed to cover.

- Office premises used wholly in a business. A suite of offices used entirely by a business (whether owned by the SMSF or leased to a related party) satisfies the test. The office does not have to be occupied 24/7 — it is the character and purpose of the use that matters.

- Factory, warehouse, or industrial shed. Manufacturing or storage facilities used wholly in a business. These are the most straightforward commercial property examples and the ruling is unambiguous about their qualification.

- Retail shop operating as a business. A shop premises used entirely for retail trade satisfies the test. The tenant can be a related party, provided the rent is at arm’s length.

- Farming land used wholly in a farming business. SMSFR 2009/1 is explicit on this one. Farmland used entirely in a farming business qualifies. There is a nuance the ruling addresses: where a farmhouse sits on the land and is used as the farmer’s residence, the ATO accepts that the farmhouse forms part of the farming business (it is where the farmer lives to work the land) — making the entire property, including the residence, business real property in a farming context. This is a narrow exception specific to farming; it does not apply to residential property generally.

- A property leased from the SMSF to a related-party business at market rent. This is perhaps the most practically important scenario. Your SMSF can buy a commercial property and lease it to your own business. That property qualifies as business real property because the underlying land is being used wholly and exclusively in your business — even though you (or your related entity) are both the landlord (via the SMSF) and the tenant. SMSFR 2009/1 para 23 makes this clear.

What does not qualify — the critical exclusions

Getting this wrong has serious consequences. If your SMSF holds property that does not genuinely qualify as business real property, you can trip over multiple compliance obligations simultaneously — the in-house asset rules, the related-party acquisition prohibition, and potentially the NALI provisions if lending is involved.

- Vacant land with no current business use. SMSFR 2009/1 is unambiguous: the land must be currently used in a business. Vacant land has no business use, regardless of its zoning or intended future use. Land banking in your SMSF is not a business real property strategy.

- Residential property. A house or unit does not satisfy the business use test. Even if someone occasionally works from home in the property, that incidental use does not transform a residence into business real property. The ATO addressed this area in paras 33–35 of SMSFR 2009/1 — residential property is excluded.

- Mixed-use property with a residential component. This is a trap. A shop-top building — commercial premises downstairs, residential flat upstairs — does not qualify as a whole. The residential component fails the wholly and exclusively test for the entire building. SMSFR 2009/1 is explicit: the entire property must satisfy the business use test. The only way to hold just the commercial part is if it is separately titled — a separate strata lot, for example. If it is a single title with both uses, the residential component taints the whole.

- Land banking and development sites not yet in business use. A development site that will eventually be a commercial building — but is not yet being used in a business — does not currently qualify. The test is about present use, not future intention.

- Property temporarily vacant between tenants. This gets nuanced. The ATO takes a practical view: a short gap in occupancy between business tenants does not automatically destroy the business real property character, provided the property has a genuine commercial character and is actively being marketed for business use. An extended vacancy, however, is a real risk — particularly if the property is then used for something other than business. This is not a bright-line rule; take advice before a vacancy situation becomes prolonged.

- Property used partly for business and partly for personal storage or private purposes. Any private or personal use, even minor, fails the “exclusively” limb of the test. Keep business use genuinely 100%.

The “commercial” misconception

“Commercial property” is a colloquial and planning-law term. “Business real property” is a legal term under s.66 of the SIS Act. They are related but they are not the same thing, and confusing them leads to compliance errors.

A property can be commercially zoned and still fail the s.66 test. Vacant commercial land is the clearest example — it is commercially zoned, but with no current business use, it has no business real property status. Conversely (and this is the farming scenario discussed above), property that might look residential in character can qualify as business real property if it is genuinely used wholly and exclusively in a business. The test is about use, not zoning.

When assessing whether a property qualifies, ignore the planning certificate. Ask one question: is this land being used wholly and exclusively in one or more businesses, right now?

How the SMSF commercial property LRBA works

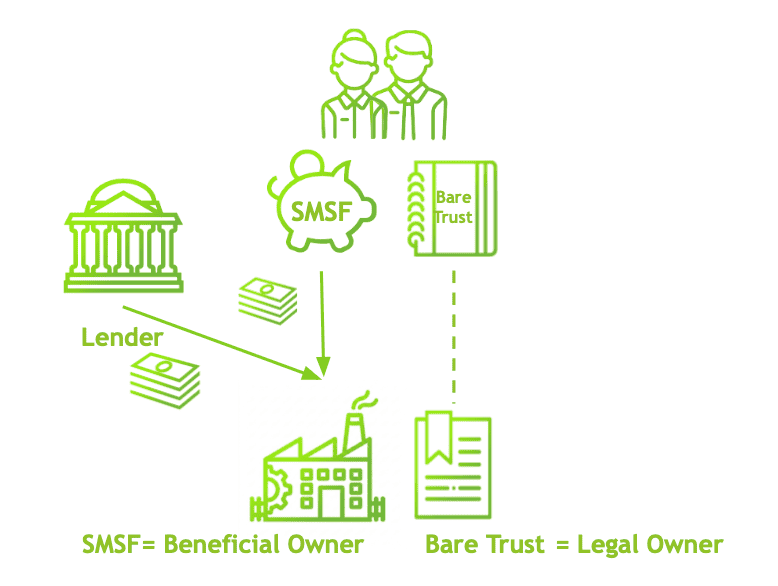

An LRBA is not a standard property purchase. The structure involves a bare trust (also called a custodian trust) — a separate legal entity that holds the property on behalf of the SMSF while the loan is outstanding. The SMSF is the beneficial owner from day one, but legal title sits with the bare trustee until the loan is fully repaid, at which point the property is transferred into the SMSF’s name.

The “limited recourse” part is critical. If the SMSF defaults on the loan, the lender’s only recourse is the property in the bare trust. The lender cannot touch the SMSF’s other assets — the fund’s share portfolio, cash, other properties, or any other investments. This asset protection is one of the key reasons the LRBA structure exists.

One compliance point that catches people regularly: the bare trust deed must be executed before settlement. The lender funds the purchase to the bare trustee, not the SMSF. If the bare trust does not exist at settlement, the SMSF has effectively acquired the asset directly and the LRBA structure has not been properly established. See our guide on when to date a bare trust deed for the full detail on this — it is a common mistake with serious consequences.

Commercial LRBA loan terms in 2026

Commercial SMSF loans attract different (and generally less favourable) terms than residential mortgages. Lower LVRs, higher rates, and more lender scrutiny on the property quality, tenant, and fund balance. Here is where the market sits as at June 2026:

| Feature | Typical range | Notes |

|---|---|---|

| Maximum LVR | 60–70% (some lenders up to 75–80%, even higher for medical/dental premises) | Commercial assets attract lower LVR than residential |

| Deposit required | 30–40% of purchase price, plus costs | Must come from SMSF cash — no personal contributions at settlement |

| Interest rate (bank/non-bank) | 7.09%–9.95% p.a. | Depends on LVR, property quality, fund size, and lender |

| Interest rate (related party) | 8.95% p.a. (2025–26 safe harbour) | PCG 2016/5 safe harbour; 9.35% for 2026–27 — see note below |

| Maximum loan term | Up to 30 years (some lenders) | Most commercial SMSF products are 15–25 years |

| Interest only period | Up to 5 years (some lenders) | Not all lenders offer IO on commercial SMSF loans |

| Loan type | P&I or interest only | Related party safe harbour requires P&I |

| Key lenders | Liberty, Pepper Money, La Trobe, Thinktank, BOQ Specialist, Macquarie | Major banks (CBA, ANZ, NAB, Westpac) do not offer SMSF loans |

Related party safe harbour rates: For 2026–27, the ATO safe harbour rate for real property LRBAs is 9.35% p.a. (up from 8.95% in 2025–26), per the methodology in PCG 2016/5. The safe harbour also requires a maximum LVR of 70%, a maximum loan term of 15 years, a registered mortgage, and monthly principal and interest repayments. See our related party LRBA safe harbour guide for the full rate table and conditions.

Note on Pepper Money rates: Following the RBA’s 0.25% cash rate increase in May 2026, Pepper Money passed the increase on to variable rate SMSF loan holders. If you are on a variable rate with any non-bank lender, check whether your rate has moved.

Minimum fund balance in practice: Most lenders want to see at least $300,000 in the SMSF. For commercial property, $400,000–$500,000 is more realistic given the higher deposit requirements. On a $1,000,000 commercial purchase, a 35% deposit is $350,000, plus roughly $70,000–$80,000 in stamp duty, legal fees, SMSF setup costs, and bare trust costs — meaning you need $420,000–$430,000 from SMSF cash before you start.

For a discussion of whether SMSF loan offset accounts are available on commercial LRBA products, see our dedicated article.

The leaseback strategy — buying your own business premises in your SMSF

This is the strategy most business owners come to Grow SMSF for, and it is genuinely one of the most powerful structures in the SMSF toolbox. The concept is simple: your SMSF buys the commercial premises your business operates from. Your business then pays rent directly into your super fund.

Think about what that means. Every dollar of rent your business pays is a tax deduction in the business. That same dollar lands in your SMSF and is taxed at 15% — or 0% once the fund is in pension phase. You are effectively redirecting money that would otherwise go to a third-party landlord (and produce no tax benefit to you personally) into your own retirement savings, with a tax arbitrage on both ends.

A few rules apply to keep this legitimate:

- Market rent is non-negotiable. Your business must pay arm’s-length market rent. Not a dollar below market. Get an independent rent assessment from a registered valuer before executing the lease. If the rent is below market, the ATO treats the shortfall as a non-arm’s-length income (NALI) issue — and NALI is taxed at 45%, not 15%. That wipes out the entire benefit.

- The lease must have commercial terms. A one-page informal arrangement is not enough. The lease needs to specify the term, rent review provisions (typically annual CPI or market reviews), outgoings allocation, make-good obligations, and renewal options. Treat it exactly as you would a lease with a third-party landlord — because from a legal and tax perspective, that is what it is.

- A related party can absolutely be the tenant. This is one of the key distinctions between residential and commercial property in an SMSF. For business real property, a member’s own business can be the tenant. This is explicitly permitted under the SIS Act. Contrast this with residential property — a related party can never rent a residential property held in an SMSF, regardless of whether the rent is at market rates.

- The SMSF is the landlord. It collects the rent, pays the loan repayments, and pays the outgoings (or passes them to the tenant under the lease terms, which is common in commercial leases). The SMSF bank account is a separate account from any personal or business account.

CGT when you eventually sell: Property held for more than 12 months in accumulation phase attracts a 15% effective CGT rate (a one-third discount on the 15% tax rate brings it to 10%). In pension phase, capital gains on assets supporting pension liabilities are tax-free — 0%. This is one of the reasons SMSF commercial property is most effective for trustees who are 10–20 years from retirement and can hold through the growth cycle.

For more on negative gearing considerations for SMSF property, see our article on negative gearing inside an SMSF.

Worked example

Here is how the numbers look on a straightforward commercial leaseback:

- Purchase price: $1,200,000

- SMSF deposit (35%): $420,000

- Loan amount: $780,000 at 7.5% p.a. interest only

- Annual interest cost: $58,500

- Market rent (6% gross yield): $72,000 per year

- Net income to SMSF (before outgoings): $72,000 − $58,500 = $13,500

- Tax in SMSF (15% on $13,500): $2,025

- Business tax deduction on $72,000 rent: $72,000 × 30% company tax rate = $21,600 saved in the business

The SMSF is cash-flow positive from year one (outgoings aside), and the business is saving $21,600 in tax on rent it was going to pay to someone anyway. If the property appreciates to $1,500,000 over 10 years, the capital gain of $300,000 is taxed at 10% in accumulation phase ($30,000) or 0% in pension phase. Compare that to holding the property personally or in a company structure — the SMSF wins almost every time.

“Your super fund collects rent from your business, your business saves tax on the rent. It compounds over time.”

Residential vs commercial property — how they compare inside an SMSF

Post-ban, the comparison between residential and commercial property inside an SMSF is not close. Here is the full picture:

| Feature | Residential property | Commercial property (business real property) |

|---|---|---|

| Can SMSF borrow via LRBA? | ❌ No — banned for new arrangements from mid-2026 | ✅ Yes — fully preserved under new s.67A(2)(c) |

| Acquire from a related party? | ❌ No — prohibited under s.66 SIS Act | ✅ Yes — permitted at market value with independent valuation |

| Lease to a related party? | ❌ No — related parties cannot lease residential SMSF property | ✅ Yes — a member’s business can be the tenant at arm’s-length market rent |

| Who pays outgoings? | Typically the landlord (SMSF) — rates, insurance, maintenance | Often the tenant under a commercial net lease — outgoings passed through |

| Typical gross rental yield | 2.5%–4.5% p.a. | 5%–8% p.a. (depending on location, tenant, lease term) |

| Typical vacancy periods | Short (1–4 weeks in most metro markets) | Longer (1–12+ months depending on property type and market) |

| Tenancy risk | Higher turnover; short leases (typically 12 months) | Lower churn; longer leases (3–10+ years) — but harder to re-let if vacant |

| Capital growth profile | Historically stronger in major cities | More variable; driven by tenant covenant, WALE, lease terms |

| Related party lease permitted? | ❌ No | ✅ Yes |

| GST applicable? | No (residential supply is input-taxed) | Generally yes — SMSF may need to register for GST; rent is GST-inclusive |

| Stamp duty concessions? | Standard residential rates | Varies by state; some states have specific SMSF or commercial rates |

| SMSF tax on rental income | 15% (lower with depreciation; 0% pension phase) | 15% (0% pension phase) |

| CGT on sale | 15% accumulation; 10% if held >12 months; 0% pension phase | Same: 15% / 10% / 0% |

| Borrowing capacity post-August 2026 | Nil — new LRBAs prohibited | Up to 60–75% LVR depending on lender |

| Minimum recommended SMSF balance | $300,000+ (unlevered purchase) | $300,000–$400,000+ (with borrowing; deposit plus costs) |

Commercial property outperforms residential inside an SMSF on almost every compliance dimension — you can acquire from a related party, lease to a related party, and still borrow. The two genuine trade-offs are vacancy risk (commercial property can sit empty for months, not weeks) and capital growth, which is less predictable than residential in Sydney and Melbourne. For most business owners, those trade-offs are worth making.

Who should (and shouldn’t) consider a business real property LRBA?

Good candidates

- Business owners currently paying rent to a third-party landlord. If your business is paying $60,000–$120,000 a year in rent to someone else, that money is gone. Buy the premises in your SMSF and redirect those payments into your own retirement fund. This is the single strongest use case for this strategy.

- Trustees with $300,000+ in the fund. You need enough cash to cover the deposit (30–40%) and the transaction costs (~7–8%). On anything meaningful, that means $300,000 as an absolute floor, and $400,000–$500,000 is more comfortable for a typical commercial property purchase.

- Funds with a well-diversified strategy that can accommodate illiquid property. Property is illiquid. Your investment strategy needs to acknowledge this and your fund needs enough liquid assets to continue meeting super obligations, paying expenses, and absorbing any cash-flow gaps between tenants.

- Professionals operating from identifiable premises. Doctors, dentists, lawyers, accountants, engineers — anyone running a practice from premises they could own. The building is an asset, the lease payments are a tax deduction, and the super vehicle is the most tax-efficient entity you can use to hold it.

Not a good fit

- Trustees who need liquidity from the fund. An LRBA property ties up a substantial portion of the SMSF’s capital. If you are close to retirement and need to draw on the fund’s assets, locking up $400,000+ in a property is the wrong move.

- Funds too small to service the loan from rental income and contributions. If the rent barely covers the interest and the fund has no other income to draw on for expenses, you are operating on a knife edge. A vacant quarter could put the fund under genuine financial stress.

- Property that does not genuinely satisfy the business real property test. Do not try to stretch the definition. Vacant land, residential property, or mixed-use buildings without separate titles — these fail the test. The compliance consequences of getting this wrong are serious, and the ATO is not lenient on arrangements that were structured to avoid the rules.

- Trustees whose primary motivation is capital growth alone. Commercial property does not consistently deliver the capital growth trajectory that residential property has historically achieved in Australia’s major cities. If capital growth is the main driver and you do not have a related-business use case, look at alternatives to direct property in super.

Compliance checklist before you proceed

Run through this before you sign anything.

- Confirm the property satisfies the s.66 business real property definition at the time of purchase. Not just theoretically — get advice on the specific property. The test applies at the point of acquisition and must continue to be satisfied ongoing. If the business moves out and the property sits vacant, it may cease to qualify.

- Get an independent market valuation of the purchase price. This is mandatory for acquisitions from related parties and is best practice regardless. The valuation protects the SMSF, establishes the arm’s-length price, and is required for the fund’s financial statements.

- Get an independent market rent assessment before executing the lease. Not an estimate from the selling agent, not a quick desktop calculation — a formal rent assessment from a qualified valuer. This is the document that protects you from the NALI provisions.

- Execute the bare trust deed before settlement. The lender funds the loan to the bare trustee. If the bare trust does not exist at the time of settlement, the LRBA structure has not been properly established. See our full guide on when to date a bare trust deed.

- If borrowing from a related party, comply with PCG 2016/5 safe harbour terms. For 2026–27, that means an interest rate of at least 9.35% p.a., maximum LVR of 70%, maximum term of 15 years, monthly P&I repayments, and a registered mortgage. Failure to meet safe harbour terms does not automatically mean non-compliance, but it means you must document arm’s-length terms independently. Non-arm’s-length income (NALI) is taxed at 45% — on all income from the property, not just the shortfall. See the related party LRBA safe harbour guide for the complete rate history and conditions.

- Review and update your SMSF investment strategy. The strategy must acknowledge property as an asset class, the illiquidity it introduces, and how the fund will continue to meet its liabilities. An investment strategy written for a share-heavy fund cannot simply absorb a property purchase without revision.

- Value the property annually. The ATO requires SMSF trustees to value assets at market value for financial reporting purposes each year. For real property, that means obtaining a market valuation — either a formal valuation report or a documented desktop assessment supported by comparable sales — at least once a year.

- Maintain a separate bank account for property cash flows. Rent comes in, loan repayments go out, outgoings go out. Keep this clearly separated from other SMSF cash flows. This is not a legal requirement per se, but it makes audit trail management significantly easier and reduces the risk of inadvertent mixing of funds.

Common questions

What is ‘business real property’ under the SIS Act?

Business real property is defined in s.66(5) of the Superannuation Industry (Supervision) Act 1993. It means a freehold, leasehold, or Crown land interest in real property that is used wholly and exclusively in one or more businesses. The ATO provides detailed guidance in SMSFR 2009/1 — notably, the business does not have to be carried on by the entity holding the property. What matters is that the underlying land satisfies the “wholly and exclusively” business use test.

Can my SMSF still borrow to buy commercial property after the 2026 LRBA ban?

Yes. The ban introduced by the new s.67A(2)(c) only prohibits LRBAs for residential property. Business real property (as defined in s.66 SIS Act) is explicitly carved out. Your SMSF can still borrow to buy office, industrial, warehouse, or retail premises, provided the property genuinely qualifies as business real property.

Can my SMSF buy a property from my business?

Yes — business real property can be acquired from a related party. This is an explicit exception to the general prohibition on SMSFs acquiring assets from related parties under s.66 SIS Act. The purchase must be at arm’s-length market value, supported by an independent valuation. Note: when assessing whether the property qualifies under s.66, the ATO tests the seller’s use of the property at the time of acquisition — so it must have been business real property in the hands of your business before the SMSF buys it.

Can my business rent premises owned by my SMSF?

Yes — and this is one of the most powerful aspects of the commercial LRBA strategy. A related-party business can lease business real property from your SMSF, provided the rent is at arm’s-length market rates assessed by an independent valuer. The lease must have commercial terms. For clarity on who counts as a related party, see our dedicated guide.

What are the safe harbour interest rates for an SMSF commercial property loan from a related party?

For 2025–26, the ATO safe harbour rate for real property LRBAs is 8.95% per annum. For 2026–27, the rate is 9.35% per annum. These rates are published under PCG 2016/5 and updated annually. Other safe harbour conditions include a maximum LVR of 70%, a maximum loan term of 15 years, monthly principal and interest repayments, and a registered mortgage over the property. See our related party LRBA guide for the full rate table and all conditions.

What happens if my business stops using the commercial property?

The property must satisfy the business real property test on an ongoing basis. If your business vacates the premises and no other business uses them, the property may no longer qualify as business real property. This creates compliance risk — particularly if the property was acquired from a related party or is subject to a related-party lease. Short-term vacancy between tenants is generally acceptable; extended vacancy is a real risk. Get advice before the situation becomes entrenched.

Ready to explore SMSF commercial property?

At Grow SMSF, we set up SMSFs and bare trusts for commercial property purchases, and we handle the ongoing administration. If you’re a business owner looking at buying your own premises, talk to us about setting up your SMSF or our bare trust service.

Note: We only set up bare trusts for clients also using our ongoing SMSF administration services — we don’t do one-off bare trusts for external funds.