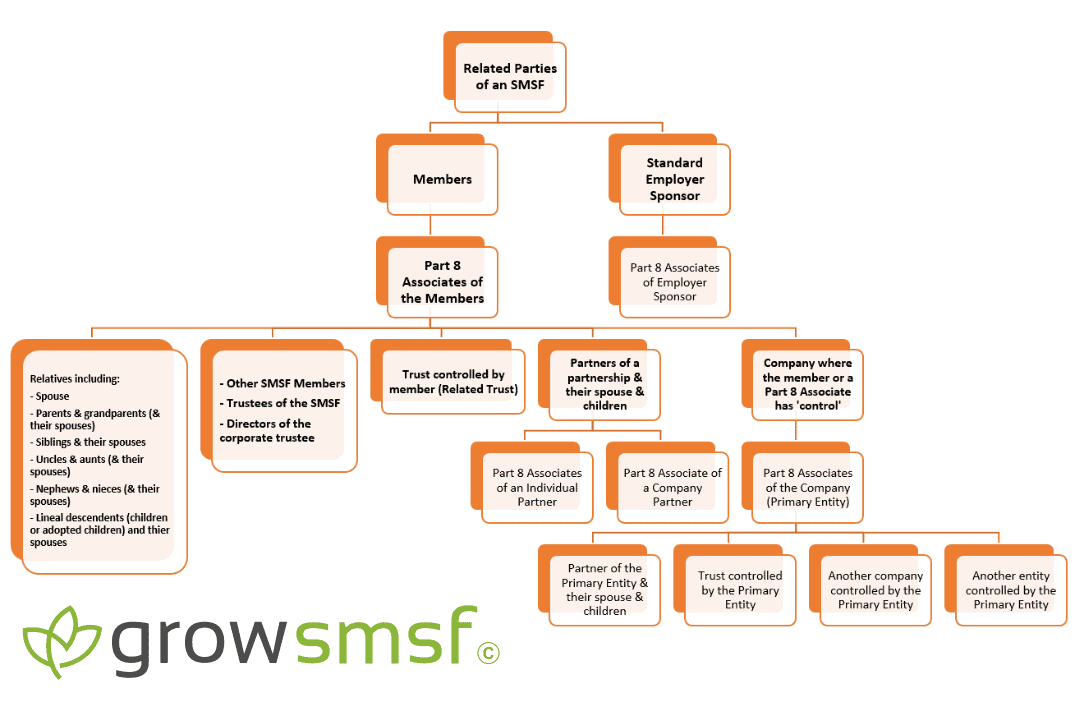

For SMSF investments, the term “related party” is relevant for the purposes of the prohibition on the acquisition of certain assets by the self-managed super fund and the in-house asset investment restrictions applicable to SMSFs. A “related party” of an SMSF means any of the following:

- a member of the fund or a “Part 8 associate” of a member

- a standard employer–sponsor of the fund or a Part 8 associate of a standard employer-sponsor of the fund (SIS Act s 10(1)).

Navigate to Key Sections

Member of an SMSF

All members of a self-managed super fund are considered related parties of an SMSF. The term “member” has its ordinary meaning. In the SIS Act, a “member” includes a person who receives a pension from the fund or a person who has deferred his/her entitlement to receive a benefit from the fund (s10(3)).

The meaning of “member” can be modified by regulations to provide that a person is to be treated, or is not to be treated, as being a member of a superannuation fund for the purposes of the SIS Act or for specified provisions of the SIS Act (s 15B).

If a superannuation interest in a fund is subject to a payment split under the family law, or a non-member spouse interest has been created under SIS Regulations reg 7A.03B, and before the payment split the non-member spouse was not a member, reg 1.04AAA provides that the non-member spouse is treated as being a member of the fund in which the interest is held for the following purposes:

- the definition of SMSF in s 17A, except s 17A(5)

- the prohibition on lending to members in SIS Act s 65

- the in-house asset rules in SIS Act Pt 8

Who is a Standard Employer Sponsor of an SMSF?

A standard employer sponsor is a related party of an SMSF. A standard employer sponsor of a fund is an employer who contributes to the fund due to an agreement between the employer and the trustee of the fund. The easiest way to determine whether an SMSF has a standard employer sponsor (who will automatically be a related party of an SMSF) is to check the trust deed of the fund.

A typical standard employer-sponsored fund would be a company superannuation fund or an industry fund covering employees. However, where an employer allows employees to select the fund to which the employer will contribute, and the employer has no other association with the fund, the fund is not a standard employer-sponsored fund. This is the case for the overwhelming majority of SMSFs. Note, however, that for the purposes of the in-house asset rules, the ATO as Regulator may also determine that a person is taken to be a standard employer-sponsor.

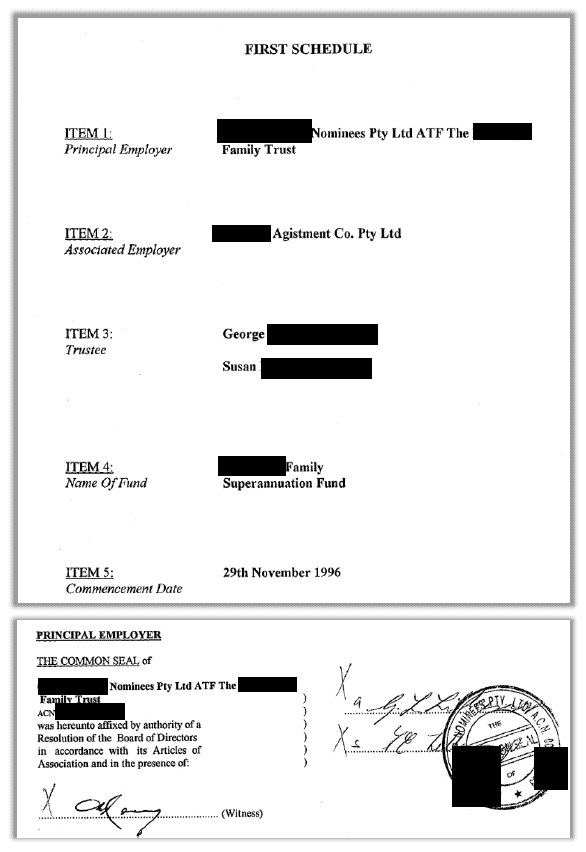

If an SMSF has a standard employer sponsor, the relationship will be noted either in the trust deed or in an attached schedule to the deed. Refer below for an example of what this looks like.

Standard employer sponsors who were noted on the trust deed were common prior to 2000, however any new SMSFs established post 2000 are unlikely to have a standard employer sponsor.

Where an employer only contributes to a fund due to an agreement between the member and the employer such as under a requirement to pay the SGC or under a salary sacrifice arrangement, they will not be considered a standard employer sponsor. In summary, an employer that pays contributions to an SMSF is NOT an ‘standard’ employer sponsor unless they are party to the trust deed of the fund or there is some other formal documented agreement.

Example SMSF trust deed pages showing an standard employer sponsor (Principal Employer):

If you have a long-established SMSF that notes an employer sponsor or principal employer of any kind, it’s important to seek professional advice about whether the employer sponsor should be removed as a part to the deed of the SMSF.

Note: In the above example, the Principal Employer may not necessarily be a standard employer sponsor. The wording of the deed would need to be reviewed to see whether the nominated employer entities are the only employers allowed to contribute to the fund.

Who is a Part 8 Associate of an SMSF?

“Part 8 associate” is defined in terms of an individual, partnership or company as the primary entity (SIS Act s 70B to 70E). In broad terms, Part 8 associates are those entities that are relatives of the individual, partners, companies that are controlled or majority-owned, or entities that control the primary entity, as discussed further below.

A separate definition of a “related trust” is used to cover an SMSF’s relationship with a controlled trust.

Who is a Part 8 Associate of an Individual?

Each of the following is a Part 8 associate of an individual member or trustee of an SMSF (the “primary entity”), whether or not the primary entity is in the capacity of trustee (s 70B):

- A relative of the individual including

- Spouse

- Parents and grandparents (and their spouses)

- Siblings (and their spouses)

- Uncles and aunts (and their spouses)

- Nephews and nieces (and their spouses)

- Lineal descendants – children natural or adopted (and their spouses)

- Other members of the SMSF

- Other trustees of the SMSF (where there are individual trustees)

- Other directors of the trustee company (where the SMSF trustee is a company)

- A partner of the primary entity or a partnership in which the primary entity is a partner

- If a partner of the primary entity is an individual — the spouse or a child of that individual

- A trustee of a trust (in the capacity of trustee of that trust) where the primary entity controls the trust

- A company that is sufficiently influenced by, or in which a majority voting interest is held by:

- the primary entity

- another entity that is a Part 8 associate of the primary entity, or

- two or more entities covered by the primary entity or a Part 8 associate of the primary entity

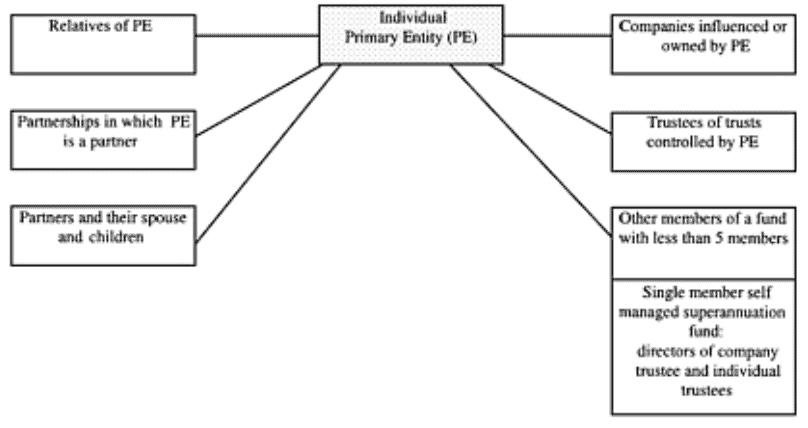

The following diagram shows the Part 8 associate of a primary entity that is an individual

What is a ‘Controlled’ Company or Trust?

Control of a company or trust comes down to “sufficient influence” and “majority voting interest”.

The expressions “sufficient influence”, “majority voting interest” and “controls a trust” are relevant for the purposes of the definition of a Part 8 associate of an individual, company or partnership.

A company is “sufficiently influenced” by an entity or entities if the company, or a majority of its directors, is accustomed or under an obligation (whether formal or informal), or might reasonably be expected, to act in accordance with the directions, instructions or wishes of the entity or entities (whether those directions, instructions or wishes are, or might reasonably be expected to be, communicated directly or through interposed companies, partnerships or trusts) (s 70E(1)(a)).

An entity or entities hold a “majority voting interest” in a company if the entity or entities are in a position to cast, or control the casting of, more than 50% of the maximum number of votes that might be cast at a general meeting of the company (s 70E(1)(b)).

An entity “controls a trust” if:

- a group in relation to the entity has a fixed entitlement to more than 50% of the capital or income of the trust

- the trustee or a majority of the trustees of the trust is accustomed or under an obligation (whether formal or informal), or might reasonably be expected, to act in accordance with the directions, instructions or wishes of a group in relation to the entity (whether those directions, instructions or wishes are, or might reasonably be expected to be, communicated directly or through interposed companies, partnerships or trusts), or

- a group in relation to the entity is able to remove or appoint the trustee, or a majority of the trustees, of the trust (s 70E(2); Interpretative Decision ID 2002/697).

For the above purposes, a “group”, in relation to an entity, means:

- the entity acting alone

- a Part 8 associate of the entity acting alone

- the entity and one or more Part 8 associates of the entity acting together, or

- two or more Part 8 associates of the entity acting together.

Example: Controlled Trust

Joe, Simone and David run a business via a partnership structure therefore the three partners are Part 8 associates of each other. Joe, Simone and David each have their own SMSF and they decide to form a fixed unit trust and issue $300,000 worth of units to each SMSF for a total of $900,000.

The fixed unit trust is a ‘controlled trust’ as Joe, Simone and David via their SMSFs are acting as a group and together have a fixed entitlement to 100% of the capital and income of the trust. The fixed unit trust is a related party of an SMSF of Joe, Simone and David and their respective SMSFs.

Example: Unrelated Trust

Same scenario as above, however instead of Joe, Simone and Davids business operating via a partnership structure, they operate under a company where each of the three owners are directors and also own 1/3rd of the shares of the company. There is no other relationship or connection between Joe, Simone and David to make them Part 8 associates of each other.

If Joe, Simone and David via their respective SMSFs established and invested into a fixed unit trust (1/3rd each), the fixed unit trust would NOT be a related party of an SMSF as each party only has an entitlement to 1/3rd of the capital and income of the trust.

Who is a Part 8 Associate of a Company?

Each of the following is a Part 8 associate of a company (the primary entity), whether or not the primary entity is in the capacity of a trustee (s 70C):

- a partner of the primary entity or a partnership in which the primary entity is a partner

- if a partner of the primary entity is an individual — the spouse or a child of that individual

- a trustee of a trust (in the capacity of trustee of that trust), where the primary entity controls the trust

- another entity (the “controlling entity”) where the primary entity is sufficiently influenced by, or a majority voting interest in the primary entity is held by:

- the controlling entity

- another entity that is a Part 8 associate of the controlling entity, or

- two or more entities covered by the controlling entity or a Part 8 associate of the controlling entity

- another company (the “controlled company”) which is sufficiently influenced by, or in which voting interest in the controlled company is held by:

- the primary entity

- another entity that is a Part 8 associate of the primary entity, or

- two or more entities covered by the primary entity or a Part 8 associate of the primary entity

- if a third entity is a Part 8 associate of the primary entity because of the above — an entity that is a Part 8 associate of that third entity

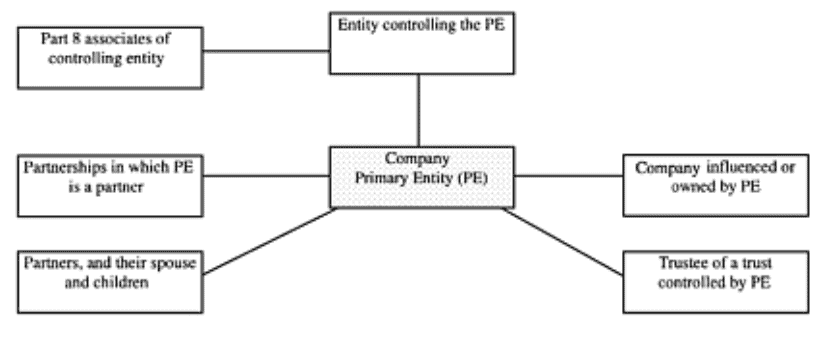

The following diagram shows the Part 8 associate of a primary entity that is a company:

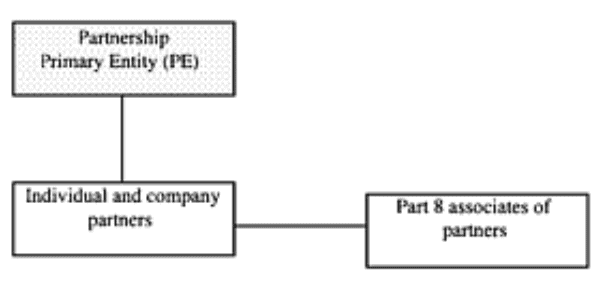

Who is a Part 8 Associate of a Partnership

Each of the following is a Part 8 associate of a partnership (the primary entity) (s 70D):

- a partner in the partnership

- if a partner in the partnership is an individual — any entity that is a Part 8 associate of that individual because of s 70B (see above)

- if a partner in the partnership is a company — any entity that is a Part 8 associate of that company because of s 70C (see above).

The following diagram shows the Part 8 associate of a primary entity that is a partnership:

Summary of Related Parties of an SMSF

The key aspect of determining who is a related party of an SMSF is to understand who are the Part 8 associates of the members and trustees of the SMSF and also who are NOT Part 8 associates.

When it comes to companies and trusts, determining whether they are related parties or not is based on ‘control’.

When a company or trust is not a related party of an SMSF, it brings significant flexibility in terms being able to borrow monies, invest in other entities and operate business (including property development) – things that cannot be achieved with a related party company or unit trust.

Questions relating to who is a related party of an SMSF

Can an SMSF rent to a related party?

An SMSF can rent ‘business real property’ to a related party, however it is prohibited from renting residential property or other assets to members of the SMSF and their related parties.

Can an SMSF sell assets to a related party?

Yes. Although there are restrictions on what assets an SMSF can purchase from a related party, an SMSF can sell virtually any investment or asset to a member of the fund or other related party provided:

- The sale is conducted on an arms-length basis and;

- The asset / investment is sold at market value

Do SMSF members need to be related?

- No, however care should be taken in terms of having unrelated members such as business partners in the same SMSF.

What is a related party loan?

- A related party loan in terms of an SMSF could be a loan made by the fund to a related party such as a member or a members business or another Part 8 associate. Loans to related parties are prohibited from an SMSF.

- A related party loan could also be a loan from the member of the SMSF (or other related party) to the fund under a limited-recourse borrowing arrangement (LRBA). This is allowable however the ATO has put in place safe-harbour provisions to ensure the loan is arms-length.

One comment

Pingback: Related Party LRBA - Safe Harbour SMSF Loan Interest Rate

Comments are closed.