⚠️ Important update — 26 June 2026: The window to set up an SMSF and purchase residential property using borrowings is rapidly closing. The bill has passed both houses of Parliament and received Royal Assent on 26 June 2026. Once granted (26 June 2026), a 45-day countdown begins — after which new residential LRBAs are permanently banned. Contracts exchanged before that deadline are protected. Read our full LRBA ban analysis →

Buying property with super has been a popular strategy over the last decade and although it’s slowed down recently, its still attractive to some. This article was originally published in early 2011 and has now been updated (September 2020) and answers common questions about buying property with super (including when you are buying property with super and borrowing and the common question: Can I use my super to buy a house?).

Navigate to Key Sections

Check out our new SMSF property solution:

SMSF property purchase name on contract

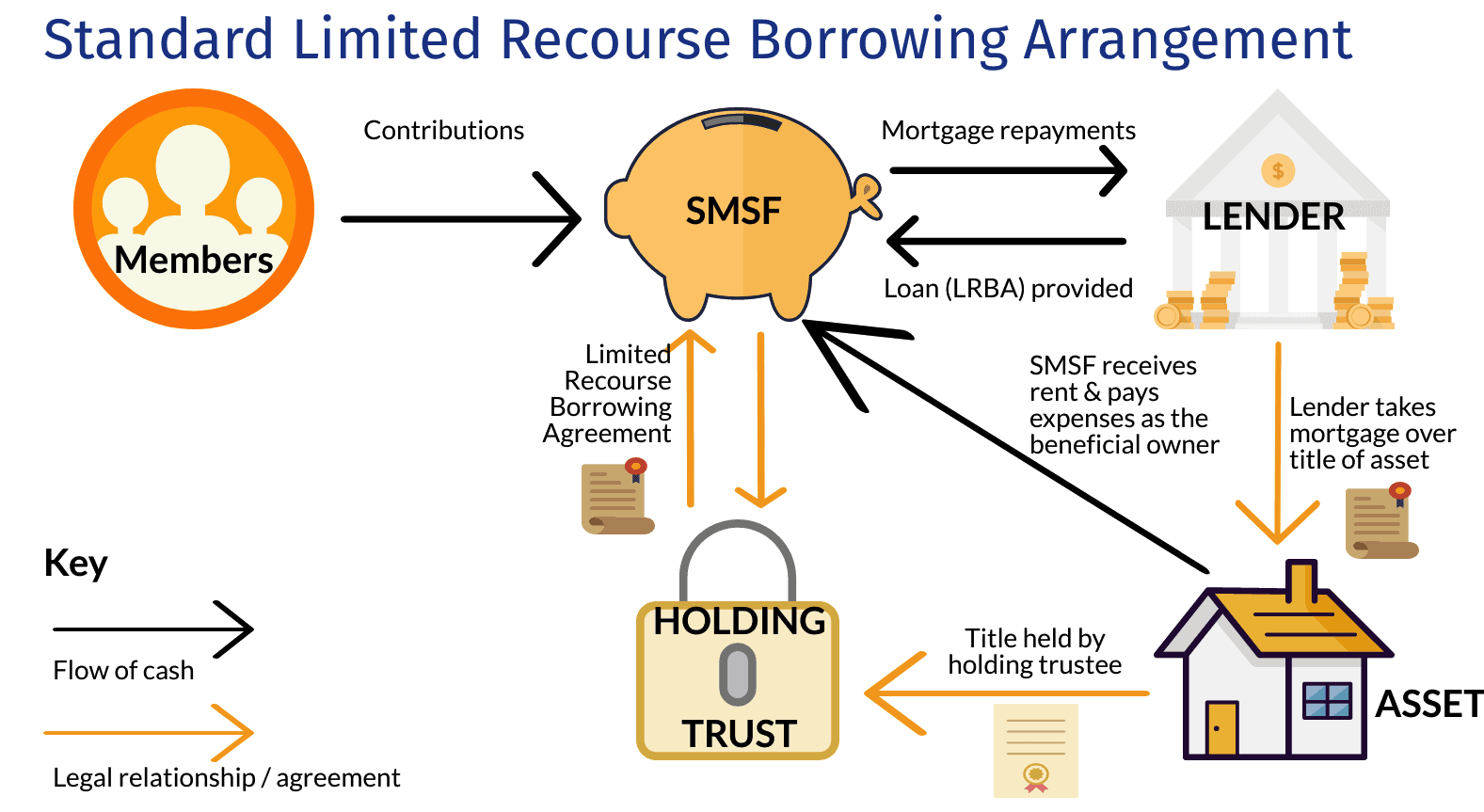

Who signs the contract of sale for a property purchased by a SMSF?

This seemingly simple question is probably the most important when buying property with super. Unfortunately this is the area that property investors (and often their advisers) seem to get wrong which is understand because the purchaser name on the contract for an SMSF purchase will vary depending on:

- The State the property is being purchased in; and

- Whether there will be an SMSF borrowing in place

The following table will tell you what name should be listed on the contract of sale where an SMSF is buying property with super.

| Jurisdiction | SMSF (No Borrowings) | Bare Trust (Borrowings) |

| NSW* | SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund | Holding Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Holding Trust |

| VIC* | SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund | Holding Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Holding Trust |

| QLD** | SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund | Holding Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Holding Trust |

| SA* | SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund | Holding Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Holding Trust |

| TAS* | SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund | Holding Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Holding Trust |

| WA** | SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund | Preferred: Holding Trustee Pty Ltd ACN XXX XXX XXX as trustee for the Name of Holding Trust for the SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund |

| ACT | SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund | Holding Trustee Pty Ltd ACN XXX XXX XXX |

| NT** | SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund | Holding Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Holding Trust as bare trustee for SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund ABN XX XXX XXX XXX |

TABLE LAST UPDATED: August 2024.

*Alternatively, the buyer’s name can simply be “Holding Trustee Pty Ltd ACN XXX XXX XXX” (as this is what will be registered on the title) without any reference to the bare trust/holding trust; however, please confirm with your solicitor for their preference.

**QLD, WA and NT purchases should sign their bare trust documents BEFORE the same day as entering into a contract.

The items in italics should be replaced by the actual company/trust / SMSF names and details.

When to date bare trust deed?

The following summarises when to date a bare trust for an SMSF property purchase:

- QLD – Before or on the contract date

- NSW – After contract date

- ACT – After contract date

- VIC – After contract date

- TAS – After contract date

- SA – After contract date but before settlement

- WA – Before or on the contract date

- NT – Before contract date

More information: When to date a bare trust deed SMSF borrowing

Bare trust / holding trust trustee company

Although individual trustees can be used a separate bare trust trustee company has the following advantages:

- The majority of banks and lenders who have SMSF loan products require a company as trustee of your custodian trust

- Property registered in the name of the company will be legally separate from those held in the personal names of the members of the SMSF

- A separate “two-dollar” trustee company adds another layer of legal protection (which is important as shown by this article: Corporate Trustee SMSF)

- The same company can be used as trustee of multiple custodian trusts

The following names should NOT be put on the contract when your SMSF purchases property utilising borrowings:

- The name of the SMSF

- The trustee(s) of the SMSF

- The members of the SMSF

- Any of the above with “or nominee”*

*Although it may still be legally binding in some states (Victoria for example) where “or nominee” is used on a contract to purchase property, it is not in others (such as Queensland). In addition I have experienced the problems it can create when the banks legal department / solicitors review the documentation.

The bare trust / holding trust trustee company MUST be set up before entering into any purchase contracts.

If you sign a purchase contract for a property with the intention of it being held by your SMSF using borrowings, and you don’t have the correct name on the contract, you will need to go back to the vendor and arrange for an entirely NEW CONTRACT to be completed with the correct name. This of course is not ideal and you may lose any leverage you have gained in the negotiation of the price and terms of the original contract.

Can an SMSF buy a block of land and build a house or develop an existing property?

Using super to buy land and then develop that land is another common question when it comes to buying property with super. So can a SMSF develop property?

A significant limitation built into the laws that enable an SMSF to borrow to purchase property is that any monies borrowed must be used to purchase a ‘single acquirable asset’.

This means you cannot do the following*:

- Buy a block of land and engage a builder to construct a dwelling or commercial premises

- Buy an existing property and develop it

- Enter into a borrowing arrangement and use borrowed funds to enter into a contractual arrangement which gives the right to a completed property – such as an off-the-plan development

- Sub-divide

*The above only applies to borrowing arrangements entered into after 7 July 2010. For borrowing arrangements entered into between September 2007 and July 2010 the above restrictions do not apply.

If you are looking to purchase an off the plan development property, you need to ensure that when the SMSF enters into the borrowing arrangement, the asset is acquiring is actually the completed property – not just a contractual right. It may simply come down to timing as often with strata-titled developments the separate strata titles do not come into existence until completion.

If you do want to use your superannuation monies with gearing to undertake some form of property development, you have a couple of options:

Commercial property (i.e. business real property): For a complete guide to buying commercial property in your SMSF using an LRBA — including current rates, the s.66 definition, and the leaseback strategy — see our SMSF commercial property loan guide.

Commercial property (i.e. business real property) — detail:

Develop the property in a different name (such as a family trust) and on completion have the SMSF purchase it. There will obviously be additional costs to be considered if using this strategy, however most state governments (except Queensland) offer stamp duty exemptions or reduced stamp duty on the transfers.

This strategy cannot be used for residential property as residential property cannot be acquired from a related party.

Development of commercial property can also use the next strategy.

Residential property:

A private unit trust can be established which the SMSF can invest into via the purchase of units, and those monies can be combined with borrowed funds to undertake the development – provided the SMSF and related parties do not own more than 50% of the total units. Another name for this structure is a ‘SUIT’ – Superannuation Unrelated Investment Trust.

To use this strategy you need to get at least one other (preferably more) unrelated parties involved – which could be friends or even business partners, however cannot be family members. It’s essential to understand who a related party is. Refer to the following article for more information: Who is a related party of an SMSF?

This strategy can work very effectively if structured and executed correctly with appropriate advice. Using an SUIT in my opinion is an underutilised, but very powerful strategy when using an SMSF to develop property. However if it goes wrong it can be an absolute nightmare – not just from an investment perspective, but also a superannuation law compliance perspective.

For further information on the related unit trust structure, please refer to my previous article: 6 ways to purchase property using your super.

How long does it take to set up?

The process of buying property with super doesn’t necessary need to take longer than purchasing an investment property in your personal names, but there are additional steps and costs and you need to get organised.

I suggest the following time frames as a n approximate guide:

- Obtain SMSF ABN (Australian Business Number ~ required for transfers of super) – up to 28 days (however in most cases when I set up an SMSF and undertake my pre-registration checks, the ABN for the SMSF is issued instantly and the SMSF is added to Super Fund Lookup within a few business days).

- SMSF receives rollover of monies from existing retail / industry super fund(s) – up to another 28 days (once again, provided all information is correct the actual time for a APRA regulated superannuation fund to process is normally 7-10 days).

- Contract date to finance approval – approximately 3-4 weeks (this does not include any delays as a result of COVID-19 which has impacted the back office operations of many banks and lenders and also assumes all relevant information is submitted to the lender is complete and accurate).

- Contract date to settlement – at least 6 weeks, stretch it to 8 weeks if possible

A lot of time can be saved by having your SMSF established and flush with cash from your rollovers before you are ready to purchase a property. Then it is simply a matter of setting up the trustee company for the holding / bare trust (the name for the contract) – which should be able to be done within 24 hours. In some cases I’ve been able to set up the holding trust and SMSF

In regards to obtaining finance (the SMSF loan) if you are self employed you will need to have two years worth of financial statements and income tax returns (business and personal) and also two years worth of superannuation statements and/or SMSF accounts to enable the bank to verify your income and super contributions.

You need to ensure your accounts and tax returns are up to date (and lodged) before signing any contracts otherwise you may find it difficult to obtain loan approval.

Similarly, if you are a wage / salary earner, you will also need two years of lodged income tax returns and superannuation statements and/or SMSF accounts.

How much can my SMSF borrow?

Depending on the lender, you can typically borrow up to 80% for residential property or 65% to 70% for commercial property. The above LVRs are subject to postcode restrictions and other lending criteria specific to the individuals banks / lenders. Importantly, the big four banks (ANZ, NAB, WBC and CBA) as well as Macquarie no longer provide SMSF limited recourse loan products. This means only smaller and second-tier lenders provide loans to this niche part of the market.

The typical minimum loan will be $100,000 and the maximums could be up to $4,000,000.

Some lenders also have SMSF loans available for rural / farm properties, however the LVR is significantly lower at 50% and also have limitations based on land size as well as location (i.e. how close to a regional town or city). This may have an impact if you are looking at buying a farm through an SMSF.

Just because you can borrow up to 80% doesn’t mean you should. My rule of thumb is no more than 65% should be borrowed, otherwise your property will likely end up being cash flow negative which will mean higher levels of capital growth will be required. In addition you need to ensure that your SMSF investment strategy has considered diversification. It may be difficult to demonstrate this diversification where the SMSF is solely invested in a single residential or commercial property. More about this here: Is you SMSF investment strategy meeting diversification requirements?

Is your investment profile up to date? Your investment profile helps us ensure your investment strategy is always suitable for your goals.https://t.co/SEEaE5B4ew

— stockspot (@stockspotcomau) April 27, 2020

Your SMSF can also borrow from yourself when it comes to buying property with super. This is called a “member financed LRBA” and there are some very strict guidelines in regards to LVR, applicable interest rates and repayment periods.

Learn more about related party SMSF limited recourse loans here.

How much does it cost to set up an SMSF to buy property?

If you have read my other articles, you know that I firmly believe that you get what you pay for. When it comes to buying property with super trying to save money upfront can end up being more costly in the long run.

The following is a general guide if you came to me and sought my assistance to buy property with your super*:

- New SMSF establishment with new trustee company – $1495 (Learn more about how to set up an SMSF here)

- Custodian trust documentation with new custodian trustee company (bare trust / LRBA) – $1,495 (note: residential property LRBAs are being banned from approximately August 2026 — see urgency notice above)

- Specialist SMSF advice from a financial adviser (where sought) – $3000 – $4000^

- Legal conveyancing – $1,000 to $2,000 depending on your chosen solicitor

- Lender legal fees and SMSF loan establishment fees – up to $1,500 – $2,500 – will vary by lender

*This above-quoted prices are subject to change and include ASIC company registration fees where applicable.

^It’s not mandatory to seek advice from a licensed financial adviser before setting up an SMSF or borrowing for property, but financial advice is often valuable.

All the above amounts are either paid for by your SMSF, or paid by yourself personally and then reimbursed once you SMSF has cash available from your rollovers.

The SMSF trust deeds and holding / bare trust documentation are all of the highest quality and have been accepted by all the major SMSF lenders.

How much are the SMSF accounting fees when buying a property with super?

Information on ongoing SMSF accounting and audit fees can be found here: Self-managed super fund fees

With Grow, the typical ongoing fee for an SMSF with property investment and LRBA is $2,275 per annum, including independent audit. In addition, the SMSF is required to pay the following ongoing regulatory fees each year:

- ATO Supervisory Levy – $259 ($518 in the first year) – paid when the SMSF lodges its annual tax return;

- ASIC Annual Review Fee – SMSF trustee company – $63

- ASIC Annual Review Fee – Bare trustee company – $310

The above fees are current as of 1 July 2023. ASIC annual review fees are indexed 1 July each year. Check current ASIC fees here: Fees for commonly lodged documents

When to date a bare trust deed?

The applicable date for a bare trust deed varies State by State.

The following summarises when to date a bare trust for an SMSF property purchase:

- QLD – Before or on contract date

- NSW – After contract date

- ACT – After contract date

- VIC – After settlement (however can be done between contract and settlement date where a nominee purchase occurs)

- TAS – After contract date

- SA – After contract date but before settlement

- WA – Before or on the contract date

- NT – Before contract date

For more information, have a look at the following article: When to date a bare trust deed for an SMSF borrowing

Buying a house with super

Can I use my superannuation to buy a house?

You can use your super to buy an investment property that can be leased to an unrelated party. You cannot use your super to buy a house for you or any of your relatives to live in. Doing so would be a severe breach of the superannuation regulations.

And before you think you can just put an unrelated person’s name on the lease and allow members of the SMSF or family members to live there, no – this will be picked up by either the auditors of the SMSF or the ATO.

Same approach for holiday rentals. If an SMSF purchases a holiday house, it must always be leased to unrelated tenants.

Buying a farm through SMSF

Can I use my super to buy a farm property?

Yes, technically, there is nothing preventing an SMSF from purchasing a commercial property that is a farm and leasing that property to either a related or unrelated business to operate the farm.

This is not a simple question, and specific advice should be sought before entering any transaction that involves buying a farm through an SMSF.

Can an SMSF purchase overseas property?

Yes. Technically it’s possible for an SMSF to purchase property in a foreign country. It’s an alternative strategy compared to buying a property with super in Australia.

SMSFs and limited recourse borrowing arrangements are uniquely Australian so if your SMSF needs to borrow to fund the purchase of overseas property, it would have to be a member financed loan (related party LRBA).

I have assisted a small handful of clients use this strategy, and it can be done, but there are a number of additional complexities / situations that need to be overcome:

- How does the purchase of overseas property fit into the SMSFs investment strategy?

- Do the trustees know what they are doing when it comes to investing in overseas property?

- How will the trustees demonstrate to the auditor of the fund as well as the ATO that the members or their families are not staying in the property?

- What are the foreign ownership rules in the country?

- An Australian SMSF or company is likely not able to be a registered owner on the title of the property – so how should the purchase be structured?

- What are the risks in terms of exchange rate fluctuations and FOREX transfer fees?

- What tax rules need to be complied with?

- Is there a double taxation agreement between the country and Australia?

- Is a foreign tax credit available to offset any Australian tax on the income (15% or 10% on discounted capital gains)?

The above list is not exhaustive. The feedback I’ve had from clients who’ve I’ve assisted in using their super to purchase, manage and sell property overseas with their SMSF has been that it’s a lot of extra work compared to owning property in Australia and they would likely not purchase overseas property again unless it was a deal that was too good to refuse!

Summary

Many people focus on property to build wealth and often look at buying inside of super via an SMSF when they’ve effectively ‘tapped out’ and the banks won’t lend them any more outside of super. This is the worse possible reason to buy a property with super. Setting up an SMSF to purchase property using super monies is NOT a strategy. It’s a transaction!

Perhaps the only saving grace of the ability to buy property with super via an LRBA is that it creates engagement. Historically most Australians, especially people under age 50 have been notoriously disengaged with their retirement savings. When the ability to borrow to buy property via super opened up, many people who didn’t give their super any thought started to take ownership and look at an SMSF earlier than perhaps they would have in the past.

This is a good thing as the biggest impediment to people growing their long-term savings (i.e. super) is apathy.

Other questions on buying property with super

If you have another question about buying property with super, please get in touch via the contact page and I can answer your question and update this article to others may also benefit and learn.

6 comments

Ted

March 12, 2011 at 1:48 am

Hi Chris,

I am still trying to get to grips with the name on the Contract of Sale and the State Revenue Office Victoria documents when an SMSF purchases a residential property.

In Victoria it may be different to other states.

Assume for a moment the following scenario:

The Smith Superannuation Fund has found a suitable investment property at 1 Fake St, Somewhere, Vic and now wants to sign the Contract of Sale. The SMSF has set up the necessary trust and trustee as companies e.g.

SMSF: Smith Superannuation Fund

Custodian Trust: Smith Bare Trust Pty Ltd

Trustee of the Custodian Trust: Smith Pty Ltd

I signed the Contract of Sale as director of Smith Pty Ltd. However, my conveyancer after consultation with the lawyer who set up the Bare Trust said that the name on the Contract of Sale should in fact be Smith Bare Trust Pty Ltd and not Smith Pty Ltd.

I then received the following documents to sign from the conveyancer:

Notice of Trust Acquisition of an interest in land (State Revenue Office Victoria).

Trust name: Smith Superannuation Fund

Trustee name: Smith Bare Trust Pty Ltd

Goods statement for residential land (State Revenue Office Victoria)

Full name: Fred Smith

Address: 1 Another St, Somewhere, Vic

Transferee: Smith Bare Trust Pty Ltd

Purchaser: Smith Bare Trust Pty Ltd as trustee for Smith Superannuation Fund

Transfer of Land (Office of Titles Victoria)

Transferee: Smith Bare Trust Pty Ltd

Executed by: Smith Bare Trust Pty Ltd

So it would seem that the purchaser is in fact Smith Bare Trust Pty Ltd and the entity signing is not the trustee of the Bare Trust but the director of the Bare Trust itself.

So it seems to be different to what you have suggested in your article. Have I or my conveyancer got this wrong?

regards

Ted

Kris_Evolved

March 12, 2011 at 11:25 pm

Yeah,

Please be aware that I am not a solicitor and I am not familiar with the intricacies of the VIC SRO and their requirements.

I would think that the purchaser name on the contract should read as follows:

“Smith Bare Trust Pty Ltd ATF Smith Bare Trust on behalf of Smith Superannuation Fund”

The SRO documents should simply have: “Smith Bare Trust Pty Ltd [A.C.N. 123 456 789]” (this should be the same in most states including QLD and NSW).

If a trust needs to be notified (as for land tax purposes etc) the trust name recorded should be “Smith Bare Trust”

I believe your conveyancer has got it wrong – Smith Bare Trust Pty Ltd is NOT the trustee of the SMSF – it is the trustee of the bare trust.

If the SMSF is noted as the trust, then what happens when you buy further properties? Your land tax amounts will be combined and the SMSF will be paying a lot more land tax than it should be if there is a separate bare trust for each individual property.

You also need to ensure that the deposit monies are paid from the SMSF. You need to be able to prove the SMSF is the beneficial owner.

An entity can’t sign anything – only a real person (the directors) can sign on behalf of an entity.

Some of the challenges you are facing are because you have not got someone who is experienced in SMSF property purchases with limited recourse loans. Whether it is me or someone else it is good to have an adviser who can assist through the entire process from SMSF set up, rollovers, contract all the way through to settlement of the property.

There are a lot of pieces that need to come together and it can be difficult even for an experienced property investor.

Ted

March 13, 2011 at 7:19 am

Hi Chris,

Thank you, you have been very helpful. Your website and articles go along way to help us SMSF newbies to understand some very complex structures.

May I seek some clarification?

In your “SMSF Borrowing 101 How to buy property with super” you say on page 13 that “…the purchaser will be the trustee company of the custodian trust.” In the Smith example previously would this mean Smith Pty Ltd purchases the property and not Smith Bare Trust Pty Ltd?

Many thanks for your time.

regards

Ted

Kris_Evolved

March 13, 2011 at 8:49 am

The purchaser is whoever the trustee of the bare trust (custodian trust) is.

Pingback: Related Party LRBA - Safe Harbour SMSF Loan Interest Rate

Pingback: When to date a bare trust deed - SMSF borrowing - Grow SMSF

Comments are closed.