⚠️ Important update — 26 June 2026: The window to set up an SMSF and purchase residential property using borrowings is rapidly closing. The bill has passed both houses of Parliament and received Royal Assent on 26 June 2026. Once granted (26 June 2026), a 45-day countdown begins — after which new residential LRBAs are permanently banned. Contracts exchanged before that deadline are protected. Read our full LRBA ban analysis →

If you’ve even wondered how you can buy property using super, this article outlines 6 alternative strategies to do so. An SMSF can be a fantastic vehicle for holding and investment property. SMSFs are extremely tax effective and provide great asset protection, however they’re not suitable for everyone or for every property. Using super to purchase property takes a bit more effort and planning compared to purchasing in your personal name, so specialist advice should always be sought.

Disclaimer: All information contained on this website is provided as an information service only and, therefore, does not constitute, and should not be relied upon as, financial product advice. None of the information provided takes into account your personal objectives, financial situation or needs, and you will need to make your own decision about how to proceed. Alternatively, for financial product advice that takes account of your particular objectives, financial situation or needs, you should consider seeking financial advice from an Australian Financial Services licensee before making a financial decision.

Buy property using super – different options

In this article I will review 5 methods of using super to purchase property including:

- Outright purchase (no borrowings)

- SMSF borrowing (limited recourse borrowing arrangement)

- Tenants in common

- Joint venture

- Unit trust

Using super to purchase property outright (no borrowings)

An outright purchase is the simplest and easiest way of buying property using super. With this option the SMSF purchases the property directly without any intermediary structures or entities in place. For this to happen the SMSF must have the ability to fund 100% of the purchase price and all associated costs.

This type of purchase is the simplest way an SMSF can invest in property. No borrowings or gearing is used – meaning the amount required is going to be a lot higher than via other methods. This limits the type of property the SMSF can afford to invest in and also could limits diversification (in either other asset classes or other properties).

A direct purchase will typically be the cheapest in terms of transaction / purchase costs – there are no other structures required to be set up.

Another advantage of an outright purchase is that there are no restrictions around developing the property, apart from the obvious necessity for the SMSF to have the necessary resources available to undertake the renovation or development.

When buying property using super as an outright purchase, typically the name of the SMSF trustee(s) should be the purchaser on the contract of sale. For example when the SMSF has a corporate trustee, the following (example) purchaser would be used: SMSF Trustee Pty Ltd ACN XXX XXX XXX as trustee for Name of Fund

It’s recommended with all options that involve buying property using super that the SMSF has a corporate trustee. More information on this here: Corporate Trustee SMSF – Individual trustees personally liable

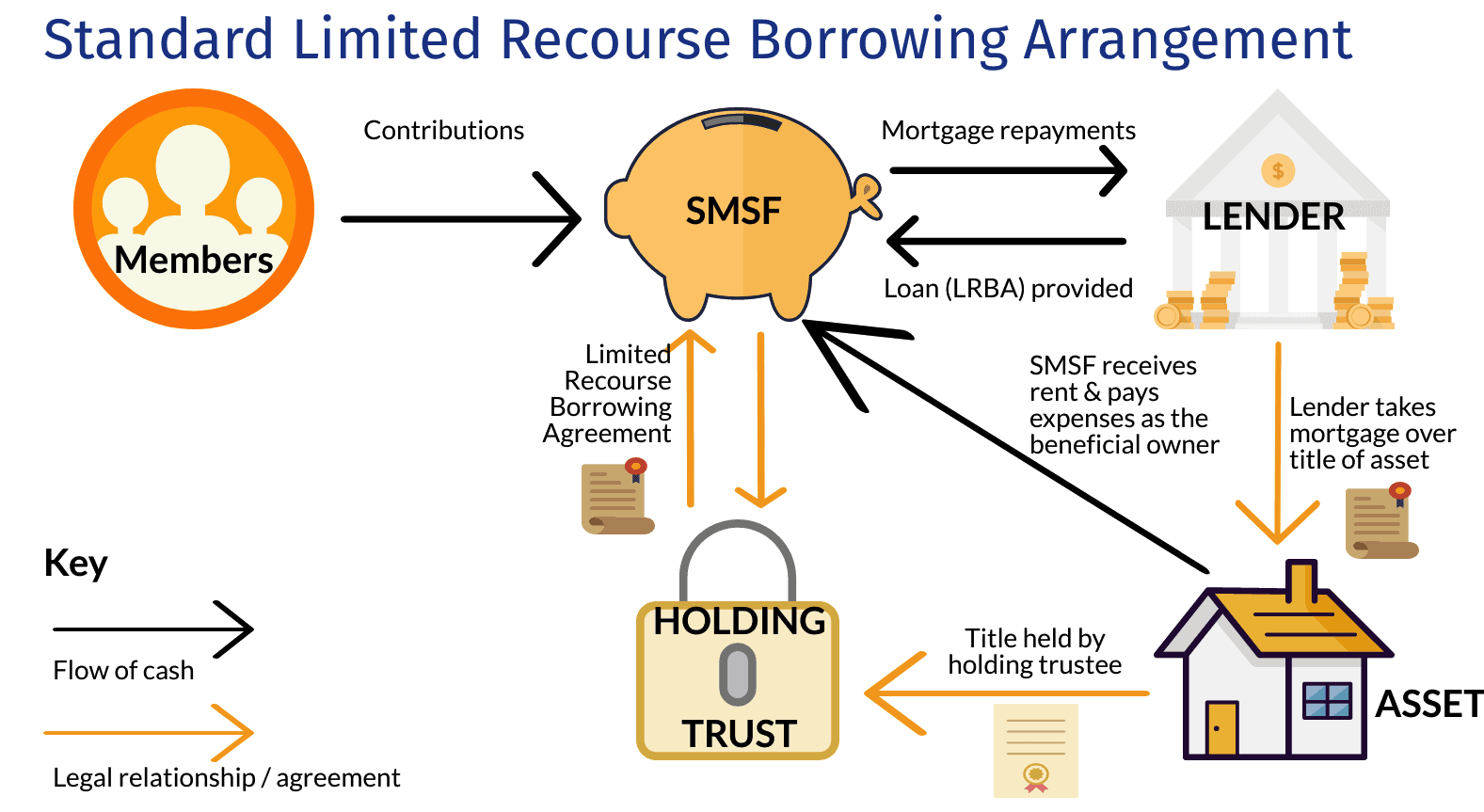

SMSF borrowing arrangement (LRBA)

This method of buying property using super involves the title of the property being legally held by owned by a simple or ‘bare’ trust (also known as a ‘custodian’ or property trust) on behalf of an SMSF. To describe it another way, a bare trust is basically a legal instrument that enables the SMSF to borrow to purchase a property – something it can only do under a limited recourse borrowing arrangement (a.k.a. installment warrant).

A limited recourse borrowing arrangement has been an extremely popular way enabling people to buy property with their super between 2010 and 2020, albeit the take up has slowed in recent years as the major banks pulled out of the SMSF loan market.

The following diagram shows the structure and flow of monies with a SMSF bare trust set up:

Although the above looks complicated, and it is more complicated compared to other ways of using super to purchase property, but the following are key aspects to understand:

- The holding trust / bare trust is a legal structure that’s required to enable a self managed super fund to buy property with super together with borrowings

- The SMSF is still the beneficial owner meaning the fund receives all the receives all the rent and capital gains and is responsible for paying the loan and all expenses

- The trustee of a bare trust can either be two or more individuals or (and most commonly) a company that holds the title on behalf of the SMSF

- The lender can be either a bank or related party of the SMSF when using super to purchase property under an LRBA but where the related party is the lender, there are strict safe-harbour requirements that need to be complied with

- Although SMSF loans are available with an Loan-to-Value ratio of up to 80% to ensure the property is cash flow positive, the LVR should be kept down to 60% – 65% wherever possible.

- SMSF loans have higher upfront and ongoing costs and also attract a premium interest rate from lenders – i.e. SMSF loans against residential property currently attract higher interest rates than standard investor loans due to their specialist nature

Once the loan is repaid the bare trust can transfer the title to the SMSF without any capital gains or stamp duty – provided it has been established correctly.

It’s important that if you are looking at using super to buy property through an LRBA structure you seek advice from a licensed financial adviser.

SMSF property purchase via tenants in common

It’s possible to use super to purchase property as tenants in common with another related or unrelated party. A tenants in common structure is where the SMSF to takes ownership of a fixed percentage of a property, with another party (such as an individual, trust or even another SMSF) owning the remaining percentage. You can have two or more owners with a tenants in common structure.

This structure doesn’t allow the title of the property to be used as security for a loan, however the other party is allowed to use borrowings provided the security is another property or other assets.

When using super to purchase property in a tenants in common structure, thought must be given to the ongoing management. The simplest way to ensure the income and expenses are split correctly to the SMSF and other parties is for there to be a joint bank account set up in the name of the SMSF and the other party(ies). This property bank account should receive all rental income and pay all outgoings and expenses. The remaining surplus cash in the bank account is then regularly transferred to the SMSF and other owner(s) based on their respective ownership percentages.

Similarly, where there is large expenditure, for example additional funds required for development or renovation, each owner will transfer the necessary cash to the joint property bank account to pay for the outgoings.

There are some disadvantages related to a tenants in common structure / joint ownership structure when using super to purchase property:

- Where the property is a residential property and one owner is a related party of the SMSF, the SMSF is unable to purchase the part of the title owned by that party (this restriction does not apply where the other party is a unrelated party);

- The property cannot be used as security for a loan, so a mortgage can never be secured against the title and an LRBA cannot be used;

- The structure is difficult and potentially expensive to unwind as it likely requires the complete sale of the property;

- The ongoing management can quickly become troublesome for the SMSF if not handled correctly – for example if the other owner (related or unrelated) either draws too much (or too little) cash from the net rental income or won’t contribute additional capital for needed repairs or renovations;

Buying property through an SMSF joint venture

A joint venture is where two or more parties form an agreement to undertake a specific commercial activity and share the result of that activity.

For example a SMSF and a family trust could pool resources / funds to purchase a block of land and build a house. On completion title would be transferred to each joint venture partner based on their percentage input (i.e. money contributed to the venture) and it would end up in a tenant in common arrangement as described above.

A very important thing to note is that the joint venture partners MUST share the outcome – i.e. the rental income of the completed property NOT the sale proceeds of the completed development.

The ATO doesn’t like joint ventures involving SMSFs – and rightly so – a lot things can go wrong. Before entering into such an arrangement professional advice needs to be sort and an appropriate joint venture agreement needs to be drafted.

If done correctly however a joint venture can be a valuable tool to enable a SMSF to enter the property development arena without entering the ‘business’ of property development – which may inadvertently lead the trustees of the SMSF to breaching of the laws that cover SMSFs.

If you are wondering whether a joint venture is an answer to the question: Can I develop property in my SMSF? the answer is ‘maybe’. Although an SMSF can develop property, there are many practicalities and rules and restrictions that must be complied with.

A correctly documented joint venture agreement however can enable a SMSF to become involved in a property development without breaching the relevant regulations that apply to SMSFs.

Unit trust to buy property using super

This structure enables two or more parties to acquire a fixed percentage of a property through purchasing units in a fixed or unit trust, where the monies are pooled and then used to purchase the target property.

Like the tenants in common structure, the underlying or target property is not able to be used as security for any borrowings. However the other investors (except for the SMSF) are able to borrow to fund their share of the purchase – provided the above restriction is not broken.

A unit trust can also issue different kinds of units that have different rights. For example there could be units which entitle the unit holder to receive a share of any income, and other units that give entitlement to capital profits or gains. This may bring advantages when using segregated investment strategies down the track.

Where a unit trust is set up and one party (or group of related investors) does not hold a controlling interest in the trust (i.e. no more than 50%) the unit trust is then able to utilise borrowings with the underlying property used as security. This is because a structure where the SMSF owns no more than 50% of the units the trust is considered to be an unrelated trust (also known as a SUIT – Superannuation Unrelated Investment Trust).

For example four unrelated parties could each invest $100k each into a unit trust, and then obtain another $500k from the bank to enable the purchase of a $900k commercial property. This is a great way for unrelated parties such as owners in a business to buy property using super.

Business owners take note: if you are looking at buying your own business premises through your SMSF, an LRBA is still fully available for commercial property. Read our complete guide to SMSF commercial property loans.

For more information please check the following article: Who is a related party of a SMSF?

Can a SMSF develop property using a unit trust? That answer to this depends on a number of factors and there are some key issues outside the scope of this article that need to be addressed. The following from the ATO provides an insight into this: SMSFs and property development

Also read: Using an SMSF unit trust to buy property with super

Buy property with super summary

Buying any property is always a big decision with high upfront costs that should not be rushed. The same applies when using super to purchase property via an SMSF.

Always ensure you get the correct advice and a structure that is appropriate for your situation if you are looking to buy property using super.

Interested in setting up an SMSF?

The following pages provides more information on how you can establish an SMSF: How to set up an SMSF

If you have any questions please contact Grow SMSF.

22 comments

Frangop

October 6, 2010 at 10:27 am

What a great article – Very informative, thank you.

Kris_Evolved

October 6, 2010 at 11:31 am

Thanks for the feedback!There is so much information out there at the moment – especially when it comes to the new(ish) super fund borrowing rules. Unfortunately most of the hard sell is coming from either property spruikers or mortgage brokers who are trying to earn a quick buck. Either they don’t understand the technicalities of how the strategies work, or how to make them work in the best interests of their clients.It is still important to realise that a great structure for investing with friends is the unit trust. It gives a lot of flexibility, but you need to have a good unit holders agreement to ensure everything runs smooth.Any other questions or comments please throw them out there.Kris

Shanerryan

January 21, 2011 at 2:29 am

Hey Kris

Great article, and like your site, thanks!

Shane, CA, Port Macquarie

Kris_Evolved

January 27, 2011 at 9:23 am

Thanks Shane.

Pingback: ATO provides further guidance on SMSF borrowing rules

Pingback: ATO provides further guidance on SMSF limited recourse borrowing rules

mick

January 27, 2011 at 6:01 am

If i purchased an investment property using my super, can I eventually use the equity in the property to purchase a home to live in or a personal investment property?

Kris_Evolved

January 27, 2011 at 9:23 am

Hi Mick,

Good question.

Yes – you can use the equity EVENTUALLY to purchase a home to live in or an investment property. The key part being – eventually – i.e. at retirement (at least over age 55 and fully retired).

To access the equity from an investment property purchased in a SMSF using a limited recourse loan, you need to sell the underlying property – you are prohibited from redraw any built up equity.

If you are looking to purchase another (subsequent) investment property pre-retirement, their is nothing preventing you from doing it under the SMSF structure again.

There are a couple of strategies I have developed that enable an investor to tip in additional savings into their SMSF and then use those amounts towards the purchase of a property, but still have the ability to take these amounts OUT of their super fund at a later date (before retirement).

I cover these strategies (and lots more) in my comprehensive guide on buying property with super which I will be releasing soon. Please ensure you are signed up to my mailing list to be notified of when the comprehensive guide is released.

I hope this answers your question.

Simoncb

March 2, 2011 at 12:40 pm

Can the person renting the investment property be the same name as holder of the super fund?

Kris_Evolved

March 2, 2011 at 9:12 pm

Residential property = no

Commercial property = yes

Simoncb

March 4, 2011 at 11:04 am

thanks for that.

would the definition of comercial property be a place of business?

Is there anyway that smsf can be used to purchase property for living in?

I am 40 yrs recently divorced, cleaned out except for the super money. It would be many years before i would be able to save for a deposit for a new house and was wondering if it was possible to access it in some way.

cheers

Simon

Kris Kitto

March 4, 2011 at 10:49 pm

Yeah – sure – go for it. Take your super money and buy a property and live in it.

That will definitely sort out your accommodation problem for a couple of years because you will be in jail.

But seriously, to answer your question, THERE IS NO (REAL / LEGITIMATE) WAY THAT A SMSF CAN BE USED TO PURCHASE PROPERTY FOR THE MEMBERS OR THEIR FAMILY TO LIVE IN !!!

The ATO has issued a rather detailed ruling on what constitutes business real property – and it is not “a place of business” – more details here: https://www.ato.gov.au/super/self-managed-super-funds/investing/restrictions-on-investments/business-real-property/

Tony

August 11, 2011 at 2:53 am

Im wanting to buy commercial land within my super fund and then build a commercial property on the land so I can run my business from it. Question: can i use a limited recourse loan to buy the land and construction of the property? Or do i need a seperate limited recourse loan for both the land and constructed property? or nether?

whats the best strategy for the above to happen. Note property is in QLD

Kris Kitto

August 12, 2011 at 7:49 am

Hi Tony

Your question is a very common one, however there is no easy answer.

One of the restrictions of using a limited-recourse loan within a SMSF (whether bank funded or funded by the members) is a little thing called a ‘single acquirable asset’. This restrictions prevents you from buying a block of land and borrowing for the construction.

As it is commercial property, you are able to purchase the land outside of the SMSF (i.e. in personal name, joint names, or a family trust etc), complete the construction and then have your SMSF purchase the completed property using a limited recourse loan.

There is also the ability for your SMSF to legitimately contribute towards the construction cost, however the details of this sub-strategy are outside the scope of my response here. I believe I cover it in my ebook (see the ebook tab on the menu above).

The downside of this strategy (especially in QLD) is double stamp duty – on the land when initially purchased, then on the complete property when acquired by the SMSF.

A second strategy is to use a reg 13.22c unit trust, where the SMSF obtains a member-financed limited recourse loan to buy units in the unit trust (not the underlying property) and have the unit trust undertake the development. This is probably a little more tricky, and the inability to utilise the underlying property as security is a major draw back.

Thanks for your question.

Kris

Sujata Shrestha

August 8, 2012 at 11:01 pm

how much amount do you need to have in your super account and how much do we have to pay as deposite

Kris Kitto

August 10, 2012 at 5:21 pm

I would suggest reading this: https://growsmsf.com.au/buying-property-with-super-common-questions/#is-buying-property-with-super-worthwhile

Cara

October 30, 2012 at 9:18 am

Hi Kris,

Can I purchase ‘land only’ through my Super fund? I am in the process of branching out and establishing a SMSF. Have searched everywhere on the internet and cannot find the info I am requiring. Thanks

Kris_Evolved

October 30, 2012 at 10:11 am

Hi Cara,

Yes, nothing wrong with purchasing land within your SMSF provided it is part of a well thought out investment strategy for your SMSF.

A couple of EXTREMELY IMPORTANT issues to consider however:

– If you need to borrow to fund the purchase you will not be able to develop / build on the land until the loan is paid off and the title is transferred to the trustee of the SMSF (rather than a custodian which needs to hold the title when the property is held under a limited recourse borrowing – LRBA)

– If you DO NOT need to borrow to cover the purchase of the land (i.e. SMSF will have enough cash to fund the entire purchase and associated costs) then you can develop the land / build on it using other monies from the SMSF.

– In either situation you CANNOT borrow to fund the construction.

The best reference for these type of questions is an ATO SMSF ruling:

http://law.ato.gov.au/atolaw/view.htm?Docid=SFR/SMSFR20121/NAT/ATO/00001

There are a number of examples including Example 9 which cover these types of deals:

_____________________________________________________________

Example 9 – purchase of land and construction of house using borrowings

The trustees of an SMSF want to enter into an LRBA where the single

acquirable asset is a vacant block of land. The SMSF intends that the

borrowing will provide sufficient funds for the construction of a house

on that block. Assuming that title to the vacant land transfers to the

holding trust prior to the house being built, it is the vacant land that

is acquired and held on trust under the LRBA .

This arrangement will cease to satisfy the requirements of section 67A if

money borrowed under the LRBA is subsequently used to construct the

house and thus improve and fundamentally change the character of the

asset held on trust (that is, from vacant land to residential premises ).

This outcome is not altered even if the contracts entered into for the

acquisition of the land and the construction of the house contain

clauses linking the two contracts .

_____________________________________________________________

There may be other options – but I don’t have enough information to determine what could be the most suitable way to obtain what you are trying to achieve.

Kris

Cara

October 31, 2012 at 3:33 pm

Hi Kris, Thanks kindly for your speedy response. It is greatly appreciated. Was wishing to know if you set up SMSF, if so – how much would it cost for me to get it done through you. How much extra would it cost, to set up a Trust and how long would this process take? kind regards, Cara

Kris_Evolved

November 1, 2012 at 9:00 am

Hi Cara,

I will answer your questions (as I believe they are common questions and it would benefit other readers to learn the answers), however as our interactions have been limited, the following should not be considered advice – it is general information only.

Apologies for not providing a short answer – but I would rather be extremely clear when it comes to potentially complex issues.

***Please also refer to additional information below my answers.***

________________________________________________________________

***Please note that any quoted fees are currently as at the date of posting this comment, and are subject to change and variation depending on the exact service offered. They should be used for a guide only.***

Yes – I can assist readers to set up a SMSF (with corporate trustee), the ‘full service’ cost is $1650 and details and the form you need can be found here, together with details of what is included:

https://growsmsf.com.au/smsf-setup/

We (Superfund Partners) generally set up SMSFs the same day we receive the order, however it can take up to 28 days (average 7-10 days) to obtain an ABN from the ATO. The ABN needs to be issued before you can request rollovers / transfers of your existing super fund monies from other super funds.

If you are entering into a borrowing arrangement, then Superfund Partners can also assist to establish the bare / custodian trust and trustee company. The current pricing is $1485.

We also offer a ‘full package’ which includes the set up of the SMSF, bare / custodian trust, financial advice and all assistance from start to settlement for $3960 – for more details please see below.

If you are 100% sure that setting up a SMSF is the right thing for you, and you have done all your research, then you probably don’t need to read any further as I have answered the questions – however I believe it will be worth your time.

________________________________________________________________

Most SMSF lenders require a financial adviser sign off prior to approving any SMSF loans – i.e. you are forced to seek independent advice prior to your SMSF borrowing (the banks are covering themselves).

For this reason we generally prefer our clients to seek financial advice around a potential property purchase within a SMSF using a limited recourse loan. This advice can be obtained independently or we can also refer you to a related adviser to assist you.

The standalone fee for this advice from our related adviser is $1650*, and is comprehensive including the following:

– Analysis of a potential property purchase, including cash flow

– Establishment of a SMSF, and also looking at alternative purchasing structure options

– Review of current superannuation accounts and advice on a rollover / transfer of benefits of a SMSF

– Insurance requirements and advice (including a review of insurances attached to your current superannuation accounts)

– The overriding focus of any advice is whether what you want to do (i.e. purchasing property in a SMSF) will actually lead to an increase in your wealth = wealth creation!

*The quoted fee is discounted 50% to $825 when you decide to go ahead to set everything up and sign a service agreement for us (Superfund Partners) to look after your SMSF administration (the $3960 total package mentioned above assumes this – i.e. $825 + $1650 + $1485).

The advice will not tell you whether should buy a specific property or buy property at all, but it will definitely provide accurate and realistic information that will ensure any investment decisions you make are well informed.

Sometimes, depending on your specific goals, setting up a SMSF without the above advice first may be putting the horse before the cart.

There is nothing wrong with determining what your options are before hand, i.e. what purchasing power you have using your super and analysing potential purchases, and when you find a property that ticks all the boxes pull the trigger and get everything set up quickly (just have a chat to us before signing any contracts!).

This method ensures you don’t prematurely incur costs that can wait.

Cara – I will email you separately with some additional information and my contact details.

Thanks

Kris

Svennis

September 4, 2013 at 10:00 pm

Hi Kris,

in the Unit Trust scenario, where the Unit Trust has a Corporate Trustee, I’ve been told that the contract of sale (of the investment residential property) must be in the name of , and signed by the Director of the Corporate Trustee.

In whose title is the property legally held? Is it the Unit Trust, or the Corporate Trustee?

Thanks!

Cecile

December 31, 2015 at 10:16 am

If you buy a property tenants in common and then subdivide and each take one block can the smsf then get a loan?

Comments are closed.