The new version of the Division 296 tax, also known as the $3 million super tax, passed the Senate on 10 March 2026 and will soon become law.

The good news? Most of the scary stuff from the original 2023 proposal has been fixed. No tax on unrealised gains. Thresholds will be indexed. And there’s now a smart one-time Division 296 cost base election that can protect pre-2026 growth forever.

I’ve been through every bit of official guidance, the revised legislation that passed both houses of Parliament in March 2026, and the latest commentary from the sharpest SMSF minds in the country and got answers to many key questions, including:

“Is the government coming after my super?”

“Will Division 296 tax unrealised gains I haven’t even sold?”

“Should I pull everything out before 30 June 2026?”

“Should I make the Division 296 cost base election?”

Let me break down the $3 million super tax in plain English, answer the questions SMSF trustees are actually asking, and give you the exact planning steps you need right now.

What Is Division 296 Tax? (And What It Definitely Isn’t)

Division 296 tax is a brand-new, additional tax that only hits individuals with total super balances over $3 million.

It is not a tax on your SMSF itself. It does not change the normal 15% fund tax or 0% pension tax inside super. And it is completely separate from your personal income tax return.

It is simply an extra 15% (or 25% in the top tier) on the portion of your super earnings that relates to the slice of your balance above $3 million. “PORTION” of super earnings that is above $3 million is key.

Think of it like this: your super already pays its normal tax. If your total super balance (TSB) across all funds is big enough ($3 million), the government wants a bit more back on the “extra” bit. That’s it.

Myth busted #1: It is not retrospective.

Myth busted #2: Division 296 does NOT tax unrealised capital gains. Only actual income and realised gains count.

When Does Division 296 Start and Who Does It Hit?

The Division 296 tax kicks in from 1 July 2026 (2026–27 is the first year).

Special rule for the very first year only: you’re only caught if your TSB is over $3 million at 30 June 2027. After that, it’s the higher of your balance at the start or end of the year.

The $3 million and $10 million thresholds will be indexed for inflation ($150,000 and $500,000 steps).

Important: Your TSB for Division 296 excludes LRBA amounts — so geared property inside your SMSF doesn’t inflate your balance for this tax.

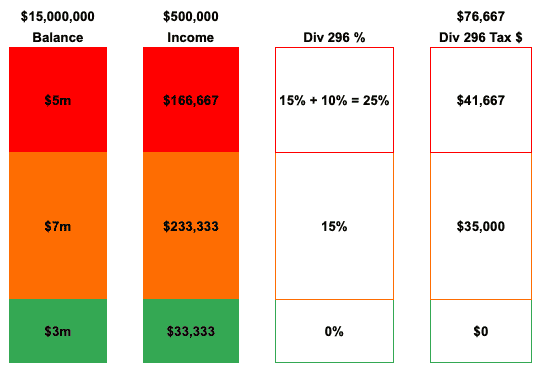

How Is Division 296 Tax Calculated? (Example)

Say your total super is $15 million and the amount of earnings allocated to your member account is $500,000 in a year (after normal fund tax).

The tax only applies to the proportion of earnings above the thresholds:

- Proportion above $3m = ($15m – $3m) ÷ $15m = 80%

- Proportion above $10m = ($15m – $10m) ÷ $15m = 33.33%

Div 296 tax payable: 15% × 80% × $500,000 = $60,000

- extra 10% × 33.33% × $500,000 = $16,667 Total extra tax = $76,667

You receive a personal assessment. Most people will use the ATO release authority so the SMSF pays it directly.

Importantly, the Div 296 tax is a completely new and separate tax applied to the individual member. The SMSF will still have its normal income tax liability calculated at the total fund level (for all members). Div 296 tax and SMSF income tax run side by side.

Some will summarise it as:

- Total tax on earnings above $3m = 30%; and

- Total tax on earnings above $10m = 40%

Original Proposal vs Final Law – Side-by-Side Comparison

The government listened. Here’s what changed:

| Feature | Original 2023 Proposal | Final 2026 Law (now passed) | Why it matters |

| What gets taxed | Unrealised + realised gains | Only realised earnings (normal tax rules) | No tax on paper gains |

| Discounting & losses | No | Yes‚ 1/3 CGT discount + losses offset earnings | Much fairer |

| Thresholds | $3m fixed forever | $3m + new $10m tier, both indexed | Keeps pace with growth |

| Pre-2026 gains | Caught | Protected via optional cost base election | Huge win |

| First year | Full year | Only end-of-year balance test | Easier entry |

Does Division 296 Tax Unrealised Capital Gains?

No. Full stop.

Only realised earnings count. Paper gains are completely safe — another big improvement from the original proposal.

Should You Make the Division 296 Cost Base Election?

This is the single biggest planning opportunity for SMSF trustees right now.

You can make a one-time, all-or-nothing election at fund level to reset the notional cost base of every CGT asset to its market value on 30 June 2026 — but only for Division 296 calculations that happen in the future. This means your SMSF will effectively have two cost-bases:

- Normal SMSF tax and capital gains;

- Capital gains calculation only for Division 296 purposes.

We expect that SMSF accounting software solutions will be updated in the coming months to accommodate the saving of the Division 296 only cost base and election.

Result: when you eventually sell, only growth after 30 June 2026 ever counts as a Division 296 earning. All pre-2026 gains are permanently protected.

Zero effect on normal SMSF tax, CGT discount or anything else.

What do the experts say? Meg Heffron has been the most direct: “Any SMSF can opt in — even one with no members who have more than $3 million in super at 30 June 2026.” In her SMS Magazine article she said the adjustment “should be considered by all SMSF members even if their total super balance is under $3 million”.

Liam Shorte (the SMSF Coach) and firms like Grant Thornton call it “cheap insurance” or “prudent forward planning”.

My take: If your SMSF has meaningful unrealised gains (especially geared property under LRBA or Bitcoin that you expect to keep growing for the next 10–20 years), the default answer is make the election unless you have a clear reason not to.

It’s important to note that unlike previous CGT elections with SMSF, the Division 296 cost base election is a the FUND LEVEL – i.e. it covers all assets inside the SMSF, even those with unrealised capital losses. For this reason, it is important to review your SMSF investment portfolio leading up to 30 June 2026 and if you have assets with unrealised gains that you no longer want in your portfolio, consider selling or otherwise disposing of these assets so the only investments remaining are those with unrealised gains which the election can be applied to.

The record-keeping is simple (just track a second set of cost bases), valuations are happening anyway for your 30 June 2026 TSB and audit, and the upside is massive protection against future threshold creep.

Special Note for Trustees Under $3m Today With Big Growth Ahead (Property & Bitcoin)

A lot of people might be sitting on an SMSF that contains property or a Bitcoin allocation that has a large amount of unrealised capital gains. You’re not over the line now — but in 10–15 years you easily could be. There are many who believe Bitcoin will exceed well over $1,000,000 USD in the future. If (or when!) the value of these assets happen, Division 296 will come into play.

So should you do the Division 296 cost base election even if you’re well below the $3 million super tax threshold?

Do the Division 296 cost base election. It costs nothing extra and locks in protection for any unrealised capital gains you’ve already built up.

Same story if you’re still making large contributions or expect strong market growth.

The Death-Benefit Scenario Everyone’s Talking About

Two spouses each with $2.8m — both under $3m individually. One passes away. The death benefit rolls to the survivor. Suddenly that person has $5.6m+ and could face a Division 296 bill.

Updated good news (March 2026 legislation): On death your TSB is set to $nil for Division 296 purposes, so there is no ongoing tax liability after death. The rollover itself is now cleaner.

Still, making the cost base election protects the pre-2026 gains from ever being caught in the survivor’s calculations. Do it.

Should You Withdraw Money From Super Before 30 June 2026?

Short answer from Meg Heffron’s modelling: almost never worth it for most people.

She ran the numbers on $7m and $15m members. Even after withdrawing enough to drop below the threshold and investing outside super at 8% pa, the long-term wealth difference was tiny (under 2% after 15 years). In many cases you end up worse off — you lose the 15% concessional environment, asset protection, and the ability to contribute back later.

Bottom line: For the vast majority, paying the extra 15–25% on the slice over $3m is still better than the alternatives. $3 million in super should now be your retirement goal — not something to run away from.

Practical Next Steps for Every SMSF Trustee

- Get your 30 June 2026 valuations sorted early (especially property, Bitcoin and unlisted assets).

- Talk to your adviser or accountant about the Division 296 cost base election before the 2026–27 return due date. Most specialists are already offering quick “should we elect?” reviews.

- Run your own numbers — especially if you have death-benefit risk or strong growth ahead.

- Document your decision (even if you decide not to elect).

FAQ: Division 296 Tax – Your Most Common Questions Answered

What is Division 296 tax? A new additional personal tax on the portion of super earnings above $3m (15%) and $10m (extra 10%).

When does Division 296 start? 1 July 2026. First year only uses 30 June 2027 balance (end of year balance).

Does Division 296 tax unrealised capital gains? No — only realised earnings under normal tax rules.

Should I make the Division 296 cost base election? Yes for almost every SMSF with unrealised gains — even if currently under $3m. It’s cheap, one-time protection.

How does Division 296 work with death benefits? Death sets TSB to $nil. The cost base election still protects pre-2026 gains for the survivor.

Should I withdraw money from super to avoid Division 296? Almost never. Modelling shows you usually end up worse off.

Does geared property (LRBA) affect the $3m threshold? No — LRBA amounts are excluded from TSB for Division 296.

Is $3 million still worth having in super? Absolutely. It should now be your goal — the tax is very manageable with the right planning.

The legislation is now final. You have time, but don’t leave the Division 296 cost base election to the last minute.

If your SMSF has any meaningful unrealised gains and a realistic path to $3m+ in the next 10–20 years (geared property, crypto, strong markets or spouse death benefits), the emerging consensus from every leading expert is clear: make the Division 296 cost base election. It’s cheap, one-time protection against future threshold creep.

You’ve worked hard to build your super. This tax is annoying, but with the right planning it’s very manageable — and $3 million in super is still a fantastic outcome most Australians can only dream of.

Need help running your specific numbers or deciding on the election? Drop us a line at Grow SMSF — we’re here to make this simple.