⚠️ Important update — 26 June 2026: The window to set up an SMSF and purchase residential property using borrowings is rapidly closing. The Treasury Laws Amendment (Tax Reform No. 1) Bill 2026 has passed both houses of Parliament and received Royal Assent on 26 June 2026. Once granted (26 June 2026), a 45-day countdown begins — after which new residential LRBAs are permanently banned. Contracts exchanged before that deadline are protected. Read our full LRBA ban analysis →

The 2026 Federal Budget as expected delivered the most significant changes to property tax rules in decades. The 2026–27 Federal Budget delivered a one-year grace period for negative gearing (restricted to new builds only from 1 July 2027 for properties acquired after budget night) and the replacement of the 50% CGT discount with an inflation-indexation model for assets bought after budget night were proved correct. SMSF 2026 budget changes outlined in this article.

While these measures will hit individual and trust investors hard, SMSFs are clear winners under the confirmed reforms — they have retained their existing one-third CGT discount. Combined with SMSFs’ unique tax concessions (15% in accumulation phase and 0% tax in pension phase), this creates a powerful relative advantage for long-term property investors. Even with the introduction of Division 296, SMSFs will still be the preferred property investment structure for long term investors moving forward.

This article explains the budget changes and why SMSFs have emerged as the preferred long term investment structure, and what forward-thinking investors should now consider as the changes have been confirmed.

The 2026 Budget Changes at a Glance

The 2026 Budget Changes – Now Confirmed (12 May 2026 @ 7.30 pm)

The 2026–27 Federal Budget, handed down this evening, has delivered the long-expected reforms to negative gearing and capital gains tax.

Capital Gains Tax (CGT)

From 1 July 2027, the 50% CGT discount that currently applies to individuals, trusts and partnerships will be replaced by inflation-based indexation, together with a 30% minimum tax on net capital gains. These changes only apply to gains arising after 1 July 2027. Investors in new residential properties will have the choice of keeping the 50% discount or moving to the new inflation-indexation method.

Negative Gearing

From 1 July 2027, negative gearing on residential property will be limited to new builds. Properties acquired before Budget night (12 May 2026) are fully grandfathered and remain completely unaffected. For established properties bought after Budget night, losses will only be deductible against rental income or capital gains from residential property, with unused losses able to be carried forward.

** Crucially for SMSFs**: The Budget explicitly states that “Properties in widely held trusts and superannuation funds will be excluded” from these negative gearing restrictions. My interpretation is that this means SMSFs can continue to negatively gear both new and established investment properties in the same way they do today.

How These Changes Will Affect Individual and Trust Investors

For individual taxpayers and trusts, the impact is significant:

- Negative gearing on established properties bought after Budget night will be restricted. Losses can no longer be deducted against salary or other income — only against rental income from that property or future capital gains. This removes one of the main tax benefits that has driven investor activity in existing housing.

- Capital gains tax on assets acquired after Budget night will rise. The move from a flat 50% discount to inflation indexation plus a 30% minimum tax means higher effective tax rates, particularly on long-held growth assets. The gap between the old and new system widens the longer an asset is held and the higher the real return.

| Situation | Negative Gearing Rules That Apply |

|---|---|

| Properties you already own (before 7:30pm 12 May 2026) | Fully grandfathered — old rules continue forever (full deductibility against other income) |

| Established residential properties bought AFTER Budget night | New restricted rules apply from 1 July 2027 (losses only deductible against rental income + carry forward) |

| New builds (regardless of when bought) | Fully exempt from restrictions — full negative gearing continues |

These changes are expected to reduce investor demand for established properties and put modest downward pressure on prices (most independent forecasts expect 3–4% softening over the next 12–18 months). However, new builds remain strongly supported through both continued negative gearing and the choice of CGT treatment. Treasury does not believe housing prices will decline, but will stop growing at such a fast rate.

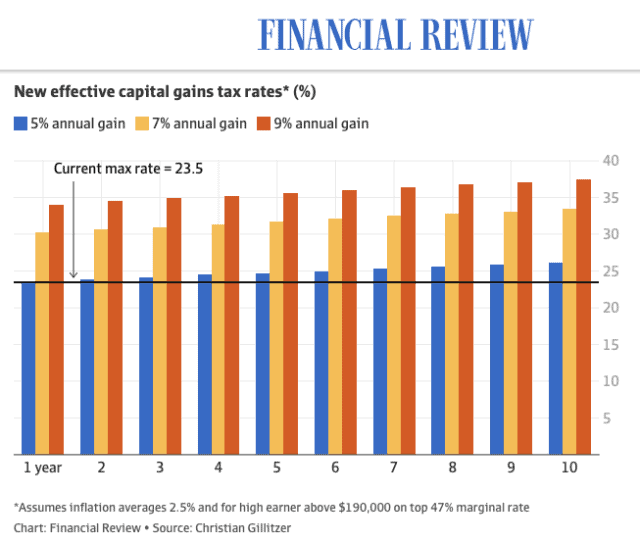

Take a typical growth asset returning 7% p.a. capital growth over 10 years, sold by an investor on the top marginal rate, with inflation averaging 2.5% p.a. Under the current 50% discount the effective CGT rate on the nominal gain is around 19.5%. Under the new indexation method it rises to approximately 27.7% (based on assumptions), but the minimum 30% net tax rate will apply on capital gains.

For a 30% marginal rate investor the gap is 15% versus 21.3%. The longer you hold or the higher the real return, the wider the penalty becomes. Indexation systematically disadvantages the very long-term, growth-oriented investors the policy claims to help — including many younger Australians.

Source: AFR – Capital gains tax to be among highest in world – May 11, 2026

In contrast, inside an SMSF the discounted CGT rate of 33.3% still applies, making the effective tax rate on capital gains on assets held for more than 12 months 10% while in accumulation phase, and once the asset (or a portion of the fund) moves into pension phase the entire gain becomes tax-free.

| Type of Asset | Negative Gearing Changes | CGT Changes | Impact on SMSFs |

|---|---|---|---|

| Established Residential Property | ✅ Yes – Restricted from 1 July 2027 (if bought after Budget night) | Yes | None – Explicitly excluded from restrictions |

| New Residential Builds | ❌ No – Full negative gearing continues | Yes – Choice of 50% discount or inflation indexation | None – Full benefits retained |

| Shares, ETFs, Crypto & Managed Funds | ❌ No – Unaffected | Yes – New rules apply | None – Retain 33⅓% CGT discount |

| Commercial Property & Other Real Estate | ❌ No – Unaffected | Yes | None – Retain 33⅓% CGT discount |

This is one of the clearest reasons SMSFs pull further ahead as a property (and share) investment vehicle after these changes. A minimum of 30% tax on discounted gains outside of super versus 10% in super (and 0% in pension phase).

Real-World Impact: What the Numbers Actually Show (non-SMSF investors)

Property bought before Budget night (grandfathered)

Consider a couple on the top marginal rate who bought an established investment unit in 2018 for $650k. They plan to sell in 2028 after ~10 years of ownership. The property is currently negatively geared by ~$8,000 p.a.

Negative gearing remains fully available for the entire holding period — the biggest practical win of the transitional design. On sale the time-apportioned CGT treatment (roughly 82% of the gain under the old 50% discount rules, 18% under indexation) produces only a trivial increase in tax compared with the pure old system. The grandfathering genuinely protects established investors.

Property bought after Budget night

Same couple, same property, but purchased in mid-2026 and sold in 2036. They can negatively gear until 30 June 2027, after which the ~$8,000 annual loss is quarantined and carried forward against future income from that same asset or the eventual capital gain. Over a decade that’s ~$80k of deductions they no longer receive in the year they incur the loss — a cash-flow hit of roughly $31k at the top marginal rate.

CGT on sale is lower than in the pre-Budget example because the entire gain is calculated under indexation. But when you net the foregone negative gearing benefits against the CGT saving, the overall outcome is materially worse for an individual investor. Add in the expected 3–4% downward pressure on established property prices and the case for buying existing dwellings weakens further.

| Period | Tax Treatment | Applies to |

|---|---|---|

| Gains up to 30 June 2027 | Old rules: 50% CGT discount | All assets |

| Gains from 1 July 2027 onwards | New rules: Inflation indexation + 30% minimum tax | All assets |

For any asset you already own on 1 July 2027, when you eventually sell it, the total capital gain will be divided into two parts:

- The portion of the gain that accrued before 1 July 2027 → taxed with the 50% discount.

- The portion of the gain that accrues after 1 July 2027 → taxed under the new inflation indexation method + 30% minimum tax.

How Do You Calculate the Split?

According to the AFR reporting (John Kehoe, 12 May 2026), taxpayers will have two options to determine the value of the asset at the transition date (30 June 2027):

- Professional valuation on or around 30 June 2027, or

- Formula-based apportionment — a specified formula that estimates the asset’s value based on its average annual return over the entire holding period, taking into account how many years were under the old system vs the new system.

The new-build exception changes everything

Newly constructed homes remain fully negatively gearable with no cap on the number an investor can hold. On sale the owner also gets the choice of the old 50% discount or indexation. For modest growth rates indexation wins narrowly; at 6%+ p.a. real growth the 50% discount is clearly superior. This carve-out is the single most valuable concession in the package — and developers will almost certainly capitalise much of that benefit into higher new-build prices very quickly.

Another consideration is that investors looking for tax benefits will spike demand for newly built properties, which could have unintended consequences such as:

- Large quantities of poor quality houses and apartments being built to meet demand;

- Oversupply decreasing prices in some areas (which is what the government is trying to achieveI guess!);

- Investors competing with first home buyers for ‘starter homes’ in Greenfield developments.

Share portfolios feel the change more acutely

An investor with a $200k share/ETF portfolio bought in 2021 and sold in 2031 (10-year hold, 7% p.a. growth, top marginal rate) faces an extra ~$7,900–$8,000 in tax purely because half the holding period falls under the new rules. For a post-Budget purchase the effective tax on the same economic gain jumps by around 42%. There is no new-build-style carve-out for equities.

Inside an SMSF in accumulation phase there is no change – the 33.3% CGT discount still applies making the maximum effective tax on gains from assets held for more than 12 months will still only be 10%. In pension phase the change becomes irrelevant — gains are tax-free. Equity investors funding growth companies therefore have an even stronger incentive to hold growth assets inside super.

the above example examples illustrate why the relative advantage of SMSFs widens after 1 July 2027.

Why SMSFs Are Clear Winners Under the 2026 Budget

- CGT treatment: SMSFs retain their existing one-third (33.3%) CGT discount. The reforms specifically target the 50% discount used by individuals and trusts. Combined with the 15% tax rate on income in accumulation phase (or 0% in pension phase), the effective tax on capital gains inside an SMSF remains dramatically lower than the new ~30%+ minimum rate that will apply to individuals.

- Negative gearing: The Budget explicitly excludes properties held in superannuation funds (including SMSFs) from the new restrictions. This means SMSFs can continue to fully deduct losses on both new and established residential properties — a major ongoing advantage. Tax losses from a negatively geared property inside an SMSF can be offset by tax deductible concessional contributions (subject to caps) by members. The strong tax arbitrage still holds.

- Pension phase remains untouched: Once assets (or a portion of the fund) move into retirement phase, all earnings and capital gains are taxed at 0%. This long-term benefit is now even more valuable.

- Overall outcome: For long-term property investors — especially those planning to hold assets into retirement — the combination of retained CGT benefits, continued negative gearing access, and the 0% pension-phase environment makes SMSFs significantly more tax-efficient than holding property in personal names or trusts.

Even if the CGT and negative gearing changes proposed for individual investors also apply to SMSFs, the overall lower income tax rates inside super still make property investment much more tax effective compared to investing in your personal name.

Negative Gearing in an SMSF — What Actually Changes

Nothing. As per the budget papers:

“Properties in widely held trusts and superannuation funds will be excluded, alongside targeted exemptions for build-to-rent developments and private investors supporting government housing programs.”

“Superannuation funds” = all complying superannuation funds, which explicitly includes:

- Industry / retail super funds, and

- Self-Managed Super Funds (SMSFs)

Why This Matters

- The government has deliberately excluded all superannuation funds from the new negative gearing restrictions on established properties.

- This means:

- SMSFs can continue to negatively gear established residential properties acquired after Budget night (losses remain fully deductible against other income within the fund).

- New builds inside an SMSF also remain fully deductible (as expected, same as new builds outside super).

- The restrictions that hit individual and trust investors only (losses only deductible against rental income + carry-forward only) and do not apply to properties held inside SMSFs.

The major tax benefits from super investors can access is tax deductible concessional contributions which reduce their personal income and tax. Concessional contribution caps are increasing from $30,000 for 2026 to $32,500 from 1 July 2026 for the 2026/27 financial year. More information here: ATO – Contribution Caps.

The Pension-Phase Game-Changer: 0% Tax on Property Gains

- Once members start a retirement-phase pension, the entire fund (or allocated portion) becomes tax-exempt.

- No CGT discount needed — zero tax on sale proceeds, rental income, or dividends.

- Ideal for long-term property investors planning to hold until (or through) retirement.

- Strategy tip: Many investors are already using SMSFs to “hold until death” or transition smoothly into pension phase to maximise this benefit.

Strategic Considerations After Budget Night – SMSF 2026 Budget

For SMSF investors, nothing changes. However we understand many Grow customers also have investment outside of super in their personal names as well as via family trusts.

- Timing: If you’ve already signed a contract before budget night, you will be grandfathered – even if you have not settled on the purchase.

- New-build carve-outs: Strong incentive to focus on off-the-plan or newly constructed properties.

- Existing portfolio: Review current holdings — grandfathering provides protection, but future refinancing or additional gearing may be affected.

- SMSF setup costs vs benefits: Upfront compliance and audit costs, but long-term tax savings can outweigh them for portfolios above ~$200k–$1m in property value.

- Professional advice: Work with an SMSF specialist accountant or licensed financial adviser before making any major decisions. And if you’re considering a residential LRBA, read our LRBA ban guide immediately — the window is closing fast.

Practical questions to ask yourself (and your professional advisers!)

- Existing investment property? Re-confirm your hold/sell thesis. The grandfathering is genuinely valuable — selling reactively now would forfeit it. But also model whether your long-term plan is to transition the asset (or the fund) into retirement phase, where future gains become completely tax-free anyway.

- Existing share portfolio with embedded gains? Don’t crystallise just to “lock in the 50% discount”. The time-apportioned transition means you keep most of that benefit on the pre-Budget portion regardless of when you sell.

- SMSF members nearing retirement? Pension commencement timing now matters even more. Gains that accrue after Budget night but are realised in pension phase remain tax-free.

- Considering geared share strategies (margin loans, debt recycling)? Review the after-tax economics on any new positions. The combination of higher CGT and (for non-SMSF investors) quarantined interest deductions changes the calculus.

- Estate planning. CGT treatment on death is unchanged — pre-CGT and post-CGT assets still pass at original cost base to beneficiaries. This reinforces the case for careful succession planning on long-held growth assets inside your SMSF.

- Trustees of family trusts. Distributions of capital gains will need to track which underlying parcels were acquired pre- versus post-Budget night. Speak to your accountant early.

- New or established property after Budget night? Purely from a tax perspective, new builds remain the strongest option outside of SMSF due to full loss deductibility and the choice of CGT treatment. For SMSF investors, established properties are still viable because SMSFs are excluded from the new restrictions (as per budget papers

“Properties in widely held trusts and superannuation funds will be excluded” ) but the relative advantage of new builds has increased for individual investors.

- Existing SMSF property portfolio? Properties acquired before Budget night are fully grandfathered. Not impacted. The CGT changes only target the 50% discount, not the current 33.3% discount applied to superannuation funds including SMSFs. SMSFs are also excluded from the negative gearing changes.

- Companies now an even more powerful investment structure: With a minimum 30% effective tax rate on capital gains and upcoming (from 1 July 2028) minimum 30% tax on distributions from family trusts, capital gains are now going to be taxed the same across individuals, trusts and companies. However, one major advantage companies (still) have is that the franking credits that build up when a Pty Ltd company pays tax are (still) refundable, meaning with careful planning, overall family tax could actually end up lower by paying franked dividends out to shareholders on lower taxable incomes. Unfortunately, Labor is killing family trusts – starting with the bucket company.

In a perfect world, tax outcomes should never be the primary driver of investment decision making. But we don’t live in a perfect world, so we need to make the best decisions at the time based on the information we have available. One this is certain: SMSF members are always ahead of the pack due to the flexibility and control offered when tax rules change, which is likely what we will see for all investors including SMSFs when the 2026 budget is released.

Is an SMSF Right for Your Property Portfolio? Pros, Cons & Next Steps Pros

The genuine positives

- The tax base did need broadening. A 50% discount that mechanically rewarded inflation rather than productive risk-taking was hard to defend on first principles.

- Grandfathering protects existing investors fairly. The political and practical case for not retrospectively rewriting decade-old decisions is overwhelming.

- The new-build carve-out provides a real incentive for fresh housing supply (even if developers capture much of the benefit through higher prices).

- Modest price relief on established dwellings (Treasury and independent forecasters expect 3–4% softening) will help some first-home buyers at the margin.

- Negative gearing losses are preserved — just quarantined and carried forward. They are deferred, not lost.

- SMSFs emerge as clear relative winners, especially for long-term buy-and-hold strategies heading into retirement.

The real concerns

- Higher effective tax on long-held growth assets disproportionately affects younger investors who, by definition, have the longest time horizons.

- Rents are likely to rise as investor demand for established properties slows and existing landlords seek higher yields to compensate.

- New-build prices will be bid up as the favourable tax treatment is capitalised in.

- No carve-out or softening for geared share and growth-equity strategies creates a genuine handbrake on the start-up and innovation sector at exactly the wrong time.

- No accompanying reduction in the 47% top marginal rate — the original driver of tax-shelter behaviour. Genuine reform broadens the base and lowers headline rates.

- Added behavioural and compliance complexity. Time-apportioned CGT calculations on existing assets will create accounting headaches and investor errors over the next decade.

Next steps: Speak to your SMSF accountant or financial adviser about a feasibility analysis. Consider whether now is the time to establish or contribute to an SMSF while rules are still favourable.

Update: Residential LRBA Ban — Window Rapidly Closing

Since this article was published, the government has agreed to ban new SMSF limited recourse borrowing arrangements (LRBAs) for residential property as part of a deal with the Greens to pass the tax reform legislation through the Senate. The Treasury Laws Amendment (Tax Reform No. 1) Bill 2026 passed both houses of Parliament on 25 June 2026 and is now received Royal Assent on 26 June 2026 from the Governor-General.

What this means for the strategies discussed in this article:

- Residential property via LRBA: No longer available for new arrangements from 10 August 2026 (45 days after Royal Assent). If you want to purchase residential property inside your SMSF using borrowings, you must exchange contracts before that deadline. Lenders may withdraw their products even earlier.

- Business real property (commercial/industrial) via LRBA: Confirmed unaffected — LRBAs for property meeting the section 66 SIS Act definition of “business real property” remain fully available.

- Existing residential LRBAs: Fully grandfathered — not affected at all, including refinancing to a new lender.

- All other SMSF strategies discussed in this article: Unaffected. The relative tax advantages of SMSFs over personal investing have increased, not decreased, since this article was published.

The window for setting up a new SMSF and purchasing residential property with borrowings is now very short. If this is part of your strategy, act immediately. Read our complete LRBA ban guide — including what to do, confirmed legislative details, and alternative structures →

Conclusion

The SMSF 2026 budget is set to reshape Australia’s property investment landscape. While individual investors face tighter tax concessions, SMSFs are positioned to become the clear winner for long-term, tax-efficient property strategies — particularly for those planning to hold assets into retirement.

Update note: This article was updated on 12 May 2026 following the official release of the 2026–27 Federal Budget.

SMSF 2026 Budget – FAQs

- Will SMSFs be affected by the 2026 negative gearing changes? No — the proposed restrictions (negative gearing limited to new builds from July 2027) mainly target individual and trust investors. SMSFs already operate under different rules (losses are quarantined within the fund and cannot offset personal income), so the impact is minimal. New-build properties will still be eligible for negative gearing inside an SMSF.

- Are super funds exempt from the new CGT rules in the 2026 budget? Yes — self-managed super funds (SMSFs) and other complying super funds have been carved out. They will retain their existing one-third (33.3%) CGT discount, while individuals and trusts lose the 50% discount and move to full inflation indexation.

- Is it better to buy property in an SMSF after the 2026 budget? For many long-term investors, yes. SMSFs gain a significant relative advantage because they keep the 33.3% CGT discount and offer 0% tax on all earnings and capital gains once the fund (or part of it) is in pension phase.

- How does negative gearing work inside an SMSF? Rental losses can only be offset against other income inside the SMSF (not against your personal salary). The fund is taxed at 15% in accumulation phase, making the net cost of gearing lower than many people realise. Limited recourse borrowing arrangements (LRBAs) for residential property are no longer available for new arrangements from 10 August 2026. LRBAs for business real property (commercial/industrial) remain available. See our full LRBA ban guide →

- What is the CGT discount for SMSFs compared to individuals? SMSFs currently receive a 33.3% CGT discount (one-third reduction) on assets held for 12 months or more. This is expected to remain unchanged after the 2026 budget, while individuals move to a less generous inflation-indexation model.

- Will the pension phase still offer 0% tax on property gains after the budget? Yes — this is unchanged. Once you start a retirement-phase pension, the allocated portion of the SMSF becomes completely tax-free. Rental income, dividends, and realised capital gains (including property sales) are all taxed at 0%, regardless of any CGT rule changes for individuals.

- Should I set up an SMSF to buy residential property using borrowings? The window is rapidly closing. The residential LRBA ban takes effect 45 days after Royal Assent — expected 10 August 2026. If you want to purchase residential property via an SMSF with borrowings, you must have an SMSF established and contracts exchanged before that deadline. Given lenders may withdraw their SMSF loan products before the legal deadline (as happened in 2019), you need to act now. SMSF setup and compliance costs are higher, but for the right fund the long-term tax advantages — especially the pension-phase 0% tax benefit — can be substantial for portfolios above ~$500k–$1m in property value. See full LRBA ban timeline and what to do →