One of the most common enquiries I receive is in relation to using super to purchase NRAS (National Rental Affordability Scheme) properties. SMSF NRAS may have been a useful strategy for some, however the NRAS scheme is now closed.

When I first heard of NRAS and how it worked I was sceptical. I asked myself “is this just a glossy, well marketed property spruik with dubious investment value?”

To answer that question, I do what I normally do – researched, asked questions and of course ran the numbers to see how they stacked up.

What is (was) NRAS?

NRAS is an Australian Government initiative which stood for National Rental Affordability Scheme, delivered in partnership with the states and territories, to stimulate the supply of new affordable, privately-owned rental dwellings. NRAS seeks to address the shortage of affordable rental housing across the nation by offering financial incentives to the business sector and community organisations, to build and rent dwellings to low and moderate income households, at a rate that is at least 20 per cent below market value rent.

The final dwellings were due to be delivered into the Scheme by 30 June 2016 and NRAS will conclude on 30 June 2026 (with no dwellings eligible to receive an incentive beyond this date).

How did SMS NRAS work?

NRAS basically works as follows:

- A developer will apply for a number of its properties in a development to become NRAS approved

- These properties will be leased to certain approved applicants (often government employed professionals such as police, nurses etc. – it is not social housing)

- The market rent is discounted by 20%

- Market rent is indexed annually based on the residential rent component of inflation

- Properties are managed by an approved manager

- Properties can be in the NRAS scheme for up to 10 years, but can be removed from the scheme and/or resold as per normal

- To compensate for the reduced rent, the investor (which can include a SMSF) receives a combination of refundable tax offsets (Federal Government) and a non-taxable State Government incentive

- The offsets and incentives currently amount to $9,524 per annum and these amounts will also be indexed annually

Please note that the above points are simply a summary. There is a lot more information available online that covers how NRAS works in a lot more detail.

What is (was) the benefit of buying an NRAS property?

Firstly, it is important to understand that an NRAS approved property is physically no different to any other property in a new development – it simply has been granted the NRAS status.

Secondly, taxation or any government incentive should never entirely drive an investment decision – sure – take them into consideration, but the underlying qualities of the investment are always the most important drivers. The same applies for NRAS investments – if the NRAS scheme was not there tomorrow, would the investment still make sense?

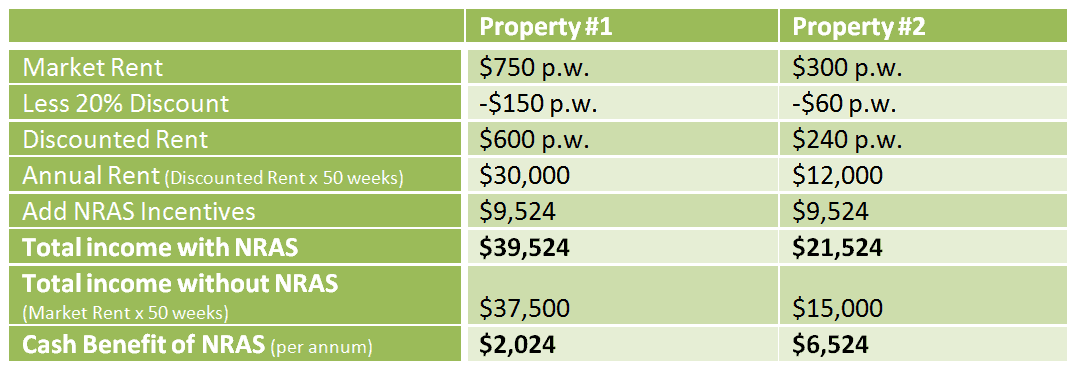

The real benefit of investing in an NRAS property compared to a normal investment property comes down to maths. The $9,524 government incentives are a flat annual amount – regardless of the property type, value and rental income.

This means the incentives have a larger positive cash flow impact on properties with a lower market rent, for example:

As we can see from the above comparison, the lower the original market rent, the greater the impact of the NRAS government incentives.

WARNING: The above is simply one factor which needs to be taken into consideration when purchasing an investment property.

An interesting point I discovered while undertaking my research is that some developers will choose specific lots / properties within their developments that will have NRAS status attached when they are purchased. The investor has no choice.

By comparison, other developers will not specify the exact lot or property, meaning they will have a certain number of different property types (houses, duplexes, terraces, units) within their developments for which they can allocate NRAS status if the investor chooses.

The latter option provides investors with a lot more flexibility and ensures you are not purchasing a discounted rent NRAS property in a group of other discounted rent properties.

How do I use my super to buy an NRAS property?

Before going down the path of using your super to purchase any kind of investment property, including an NRAS property, you need to do the following:

Read these articles:

- How much is needed to set up a SMSF

Before even setting up a SMSF or committing to any property purchase, you should already have a very good understanding of how much you will need to have in your SMSF to complete the purchase, and what the ongoing cash flow situation of the property will be.

Rather than providing significant detail in this article in regards to the actual process you need to follow (tested by me with numerous clients with a 100% success rate), I again recommend you read my free SMSF Borrowing 101 guide.

The key difference between a NRAS property investment within a SMSF and a normal property purchase comes down the available lenders.

SMSF NRAS loans property purchases

With limited recourse SMSF loans, there are a limited number of lenders available. When you combine this fact with available lender for NRAS properties, the pool of lenders shrinks dramatically.

Based on my research, there are three, maybe four lenders who even have a policy on NRAS SMSF loans. It is also important to note that some lenders will not lend on certain properties from specific NRAS consortiums.

The following is a summary of important considerations / criteria that you need to be aware of when it comes to applying for a SMSF loan for an NRAS property:

- All lenders will require a letter / sign off form from a financial planner that you have been advised on all relevant aspects of buying a property in your SMSF (this basically means you must have a financial planner prepare a Statement of Advice / financial plan specific to your property investment)

- With NRAS properties, or any new off the plan property for that matter, a bank valuation may be up to $30,000 less than the contract price – the assumption being this is the amount of marketing costs built into the final completed property

- The lenders will generally include only 80% of the discounted rent (i.e. 80% x 80% = 64%)

- The $9,524 annual government incentives are typically ignored when the lender is looking at the SMSFs ability to service the loan

- Contributions income (employer contributions and salary sacrifice) can be used in the serviceability calculations if needed

- Maximum loan amount is 80% of the property value (assume the value is up to $30,000 than the advertised price / contract price)

The above criteria a significantly different to the expected cash flow outcome of an NRAS property investment within a SMSF. The impact of the above is that you may need significantly more money with your SMSF to complete the purchase of an NRAS property than you might expect at first glance – this is why it is so important to do your research, crunch the numbers and always seek competent specialist advice.

Does an SMSF NRAS investment make sense?

If you have read my other articles, you will know that I am obsessed with cash flow positive investment as a key wealth building tool.

What I like about NRAS property investments is that they can boost the amount of cash flow generated from a property – which is fantastic. What I don’t like is slick marketing which may potentially mislead investors – this is why I want to provide you with the tools and information you need to make an informed decision.

5 comments

Liam Shorte

April 10, 2012 at 12:14 pm

Well written blog entry Kris.

Kris_Evolved

April 10, 2012 at 1:15 pm

Thanks Liam

However I believe that I have only scratched the surface.

I would really be interested to hear peoples experiences, good, bad or ugly!

Brock Chewings

September 17, 2012 at 10:51 am

Thank

you for such an informative post. This will really helps you to have a

knowledge in SMSF.

Kirsty Bonner

March 3, 2013 at 11:35 am

Thanks,this is just the article I was looking for. 🙂

Danielle

March 22, 2013 at 8:58 pm

Based on my research, there are three, maybe four lenders who even have a policy on NRAS SMSF loans.

Hi are you able to tell me what banks these are. 🙂

Comments are closed.