One of the key decision you need to make when you set up an SMSF is whether to use a corporate trustee vs individual trustees. Many online providers will default to setting up an SMSF with individual trustees to make the establishment cost cheap or free, however this is not always the best choice of SMSF trustee.

Similarly, many advisers and SMSF specialists will default to a corporate trustee which is generally a superior option, however the decision on corporate trustee vs individual trustee should be made based on all the relevant facts applicable to your situation.

It’s important that you set up an SMSF the right way to ensure you don’t run into problems and additional costs and paperwork in the future.

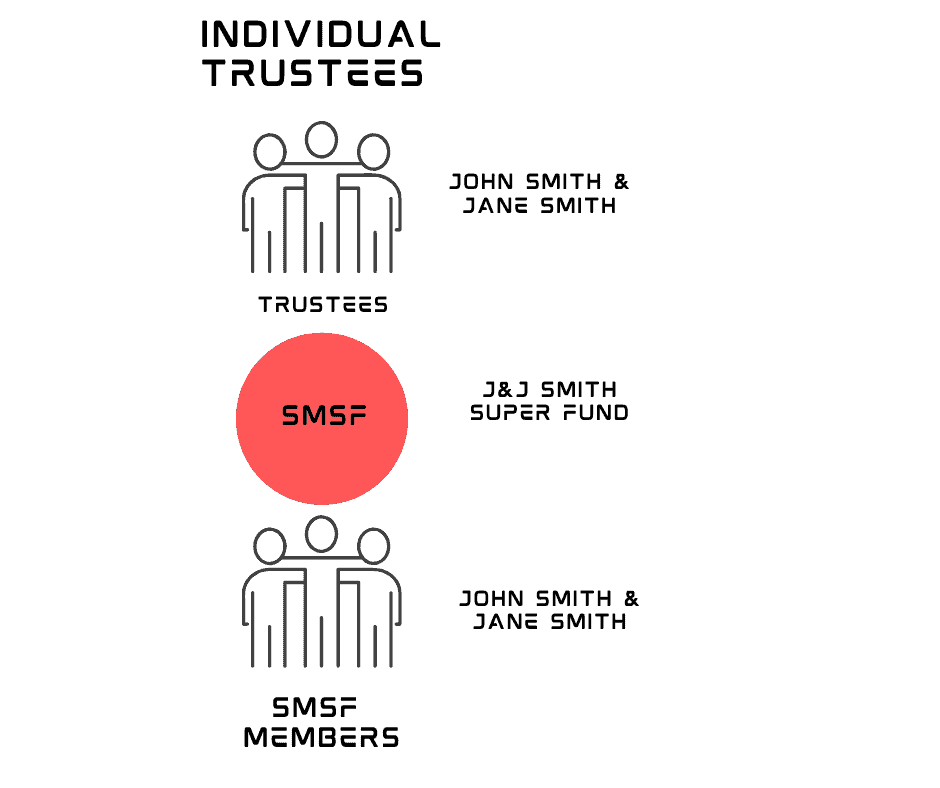

Individual trustees of an SMSF

As per the above diagram, two or more individuals can be the trustees of an SMSF. Bank and investment accounts are set up in the name of the trustees as trustee for the SMSF, for example: John Smith & Jane Smith as trustee for J&J Super Fund.

Advantages of individual trustees for an SMSF

There following is a summary of advantages and disadvantages of having individual trustees of an SMSF:

| Advantages | Disadvantages |

| Nil upfront and ongoing costs | Less liability protection for trustees personally |

| Faster and simpler SMSF set up | All investments must be changed if members change |

| Suitable for SMSFs with simple investments | If trustees fined by ATO, each trustee must pay |

| Suits SMSFs where members are a couple | Does not suit single member SMSFs |

| Potential intermingling of personal assets and SMSF assets |

The following indicate that an individual trustees may be suitable when deciding corporate trustee vs individual trustees for an SMSF:

- The investment strategy and investments are likely to be restricted to simple assets including: cash, term deposits, listed shares, managed funds and ETFs (i.e. NOT direct property)

- The SMSF is not borrowing (including to buy direct commercial or residential property)

- The membership is made up of a two individuals who are a couple (in a spousal relationship) and is unlikely to change in the long term – i.e. other members will not be added or removed from the fund

- If one of the members exits the fund (for example through death or divorce) it’s likely the SMSF will be closed rather than continue as a single member fund

Although it is cheaper to use individual trustees when setting up an SMSF, cost should never be a determining factor when choosing the most appropriate trustee structure. In most cases an SMSF will operate for many decades, so the cost of setting up a trustee company is very low when spread across 10, 20 or 30 years.

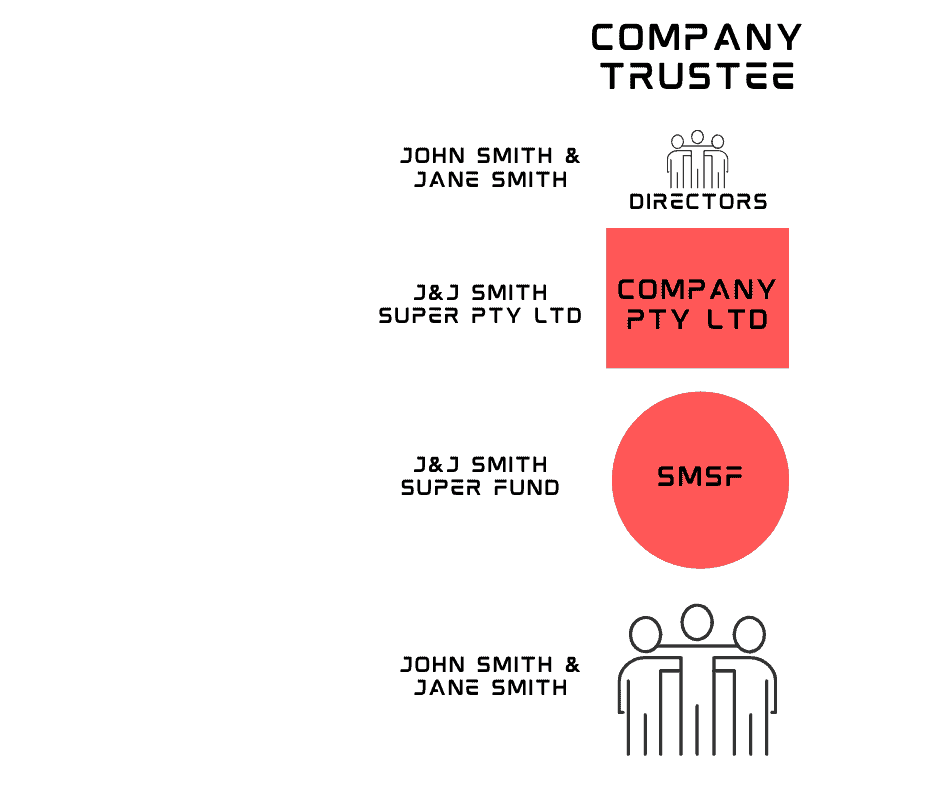

Company trustee for an SMSF

As shown the in above diagram, a ‘special purpose’ proprietary limited (Pty Ltd) company is set up to act as the trustee of the SMSF. Bank and investment accounts are set up in the name of the trustee company as trustee for the SMSF, for example: J&J Smith Super Pty Ltd as trustee for J&J Super Fund.

Advantages of a company trustee for an SMSF

There following is a summary of advantages and disadvantages of having a company trustee of an SMSF:

| Advantages | Disadvantages |

| Liability protection for the SMSF members as individuals (Read more here). | Initial upfront and minor ongoing costs |

| Slightly more complex SMSF set up process | Additional administration to keep ASIC updated (minor) |

| Suitable for SMSFs with more complex investments including property | Some investment account application and set up processes may be slightly more tedious |

| Suits SMSFs where members are a not just a couple (multi-generation or other relationships) | Some providers charge additional ongoing fees to act as a registered agent (ASIC) or to be the registered office |

| ATO fines only issued once to the company trustee | Minor additional cost and additional paperwork to de-register the company when the SMSF is closed |

| Often required by lenders for SMSF loans | ASIC late fines many apply when annual registration fees are missed or paid late |

| When members change accounts and investments stay in the same name | |

| Enables single member SMSFs | |

| Electronic signing of SMSF trust deed possible (legislation in draft – October 2020 – learn more) |

Some of the above are also covered in our other article: Reasons you need a special purpose trustee company for your SMSF

The following indicate that a company trustee may be suitable for an SMSF:

- The investment strategy and investments are likely to be restricted to more complex including: direct residential or commercial property

- The SMSF will borrowing (including to buy direct commercial or residential property) using a limited recourse borrowing arrangement (LRBA)

- The membership is made up of individuals who are not in a spousal relationship including relatives, children or parents, friends, business partners etc

- The members of the SMSF are likely to change in the future, for example including children as members (both as minors as well as when the are adults over 18)

- If one of the members exits the fund (for example through death or divorce) it’s likely the SMSF will continue running as a single member fund

In summary, when looking at corporate trustee vs individual trustee SMSF, a company trustee in most cases going to provide you a superior long-term solution compared to individual trustees for your SMSF.

SMSF trustee company set up and ongoing costs

The only practical disadvantage of using a special purpose company trustee vs individual trustees SMSF is cost.

As of 1 July 2023, the cost of registering a new company with ASIC is $576, and most providers add their professional fees to that amount making the typical additional upfront cost of a SMSF trustee company between $700 and $1200. The ongoing cost a special purpose company that only acts as trustee of an SMSF is $63 per annum from 1 July 2023. This fee is discounted compared to the $310 per year for a standard proprietary limited company that trades or acts as a trustee of a family trust for example.

One method to easily reduce the ongoing costs of a trustee company of an SMSF is to prepay the ASIC annual registration fees for 10 years. This cost is $436 from 1 July 2023 for a special purpose SMSF trustee company and considering the fees are indexed by ASIC each year, it will save approximately $200 over 10 years. In addition the likelihood of being fined late fees for not paying the annual registration fee on time is removed. The current late fees are $93 if payment is late by up to one month, and $340 if more than one month late.

All ASIC company fees for a trustee company are paid by the SMSF.

For a full list of ASIC fees applicable from 1 July 2023, visit the ASIC website: Fees for commonly lodged documents

Can the trustee be changed after set up?

Yes. Changing the trustee of an SMSF is possible. You can change from individual trustees to a company, and also from a company to individuals. A change of trustee is typically undertaken by either a lawyer or specialist SMSF provider.

A Deed of Appointment and Removal document is normally prepared which all members and trustees sign, then the investments and accounts are moved into the name of the new trustee(s).

The complexity of the process will typically be dependent on the investments and accounts the SMSF holds. In all cases professional advice should be sought because if not completed correctly could create a number of compliance problems.

Changing the trustee of an SMSF does not trigger any capital gains as the beneficial owner (i.e. the SMSF) is unchanged.

Summary

When making the important decision on corporate trustee vs individual trustees SMSF then most people are better suited to using a special purpose trustee company for their SMSF.

Individual trustees should only be used by exception when the investments are going to be (and stay for the life of the SMSF) simple and the membership is NEVER going to change (cannot be guaranteed!).

An alternative view is that you setup your SMSF with individual trustees and change it in the future. The advantage short-term is cost savings however long-term to cost and time to change could outweigh the savings.

If you have any questions please get in touch. If you’re ready to setup your new SMSF, you can do so quickly and easily online here: SMSF Set Up

4 comments

ian schuster

June 4, 2023 at 1:39 pm

Hi great read very easy to read & understand , i will be engaging an acoountancy firm to create a SMSF from my own retail super fund with my wife as a trustee also to purchase a property with a view to move into come retirement in 5 years but will before then renting it out as a rental property or air bnb .I am leaning towards a individual trust & the reasons are

1) will only have 1 property relatively simple

2) only me & my wife as trustees

3) not long term no more than 5 years.

I cannot see why we would need a company trustee arrangement ,we will strickly adhere to the trust terms & conditions so defaulting wont happen & I cannot see where or why we would be fined if we adhere to the rules.

Im not trying to save on fees or costs i just dont think that going through the process of a company trustee is required when I think ( in my view anyway ) that 1 property would be a relatively simple operation.

I dont know I would value your opinion as I am a little “not really sure which way to go “.

Kris Kitto

June 5, 2023 at 9:12 am

Have you thought about the following issues?

Example 1: You engage a tradesperson to do some work on the property, they get injured and it’s found that the trustees of the SMSF as owners were negligent. SMSF trustees are sued, insurance doesn’t cover the claim, you as the trustees are liable and YOUR PERSONAL ASSETS BECOME EXPOSED.

Example 2: You AirBNB the property. Someone injures themselves and takes action against you as the property owner. Your personal assets as trustees are again at risk.

By contrast, if a company trustee is sued, the liability is limited to the assets of the company, which could be as low as $2.

As a lawyer puts it: “In the event the SMSF (or its trustee) is sued for damages (ie if someone is injured on SMSF property) a corporate trustee may limit the exposure of liability, whereas individual trustees may have their personal assets exposed.”

You don’t think it can happen? It can. Have a read of the following article published in the AFR: Case highlights need for public risk insurance

Why would you take the risk? You wouldn’t. No rational person would.

The cost is negligible: It’s $576 for registering a new company from 1 July 2023. Ongoing fees currently $63 per year. So less than $1,000 across 5 years.

My final point is: If after reading this blog, plus this commentary and the article I linked above, if you still think it’s a good idea to use individual trustees rather than a special purpose trustee company, please DO NOT engage Grow SMSF to assist you with your SMSF. We care about our clients and hate seeing them put themselves and their assets at risk unnecessarily!

Alex Nicholson

April 30, 2025 at 10:29 am

I’ve managed two investment properties under my own name (not SMSF) and held landlord’s insurance for both. This insurance will protect you against for personal injury and other events for which the landlord might be liable. The risk is therefore mitigated through the use of an appropriate insurance policy.

Kris Kitto

April 30, 2025 at 1:37 pm

Yes, agree on that point Alex.

However it does require the insurance claim is accepted, which is likely provided there is no negligence on the part of the landlord, but if for any reason the insurance doesn’t pay and the SMSF has individual trustees, then they will become liable.

It’s almost a moot point in regards to trustee options when it comes to property. A large % of SMSFs that buy property are borrowing to do so, and most SMSF lenders require a corporate trustee.

I personally don’t have any issue with a selection of individual or company trustees. I only hope trustees make an informed decision.