Catch up concessional contributions (also known as carry-forward concessional contributions) give SMSF trustees a simple way to use unused before-tax contribution room from the past five years.

For years the rule was “use it or lose it”. Since 1 July 2018 you can roll over any unused concessional cap for up to five years — provided your total super balance was under $500,000 on 30 June of the prior year.

This guide shows exactly how catch up concessional contributions work for the 2025-26 financial year (ending 30 June 2026), with practical SMSF steps, a worked example in table form, and Grow Portal shortcuts.

Catch Up Concessional Contributions Rules 2025-26

- Concessional contributions = employer Super Guarantee, salary sacrifice and personal deductible contributions.

- Annual cap for 2025-26 is $30,000.

- Add any unused cap from the previous five years.

- Eligibility test: Your total super balance must have been below $500,000 on 30 June 2025.

Important date: Unused cap from the 2020-21 year expires on 30 June 2026. This is your last chance to use it.

Why Act Now on Catch Up Concessional Contributions SMSF

We are already deep into 2025-26. Any 2020-21 unused room disappears in a few months.

Higher earners and business owners can slash taxable income at their marginal rate while the SMSF pays only 15% contributions tax.

Example – unused caps carried forward

| Financial Year | Concessional Cap | Amount Contributed | Unused Cap |

|---|---|---|---|

| 2020-21 | $25,000 | $13,639 | $11,361 |

| 2021-22 | $27,500 | $13,629 | $13,871 |

| 2022-23 | $27,500 | $10,405 | $17,095 |

| 2023-24 | $27,500 | $14,976 | $12,524 |

| 2024-25 | $30,000 | $17,600 | $12,400 |

| 2025-26 | $30,000 | ??? | ??? |

| Total unused | — | — | $67,251 |

Using the above example, on top of the $30,000 current cap you could contribute up to $97,251 in concessional contributions (less any employer contributions made during the year) by 30 June 2026 and claim the full tax deduction.

We have also created a basic Google Sheet calculator to assist you in calculating the total available catch up concessional contributions you can make to your SMSF for the 2025/26 year:

Google Calculator – Unused Concessional Contributions 2025/26

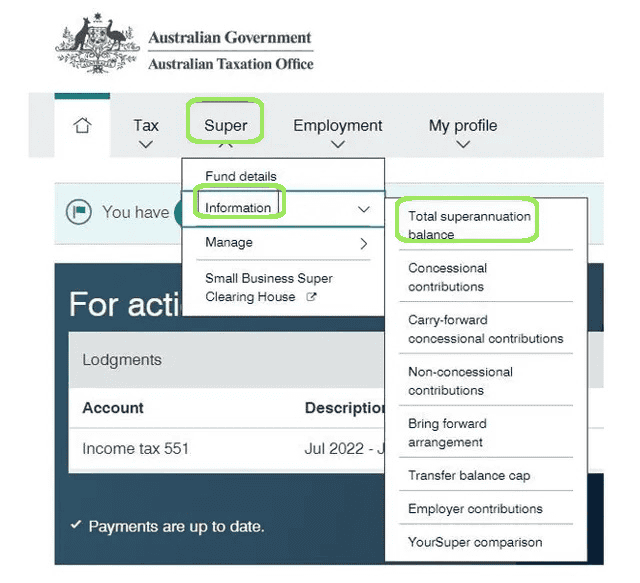

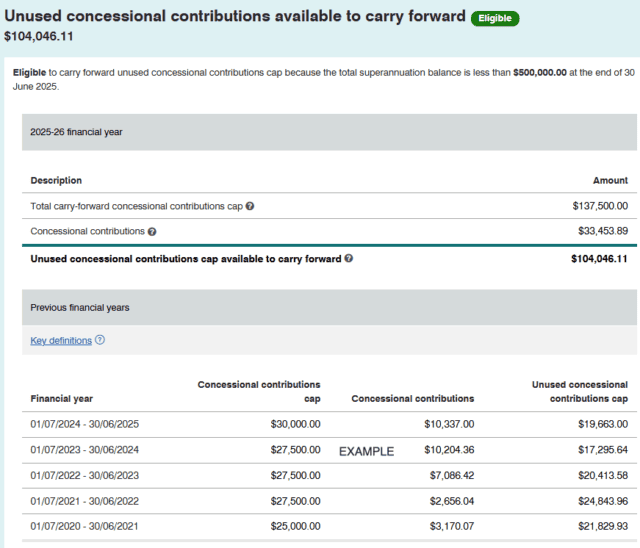

How to Check Your Catch Up Concessional Contributions SMSF Space

- Log into myGov → ATO services.

- Go to Super → Information & Details → Carry-forward concessional contributions.

- You will see the year-by-year breakdown and total available.

The screen shows only prior-year unused amounts. Subtract any 2025-26 contributions you have already made.

How SMSF Trustees Make a Catch Up Concessional Contribution

- Deposit funds into the SMSF bank account (clear reference: “Concessional contribution – [Member Name]”).

- Complete a Notice of intent to claim a deduction.

- Give the notice to the trustees before you lodge your tax return (or before the end of the next income year).

- Trustees must acknowledge receipt in writing.

Grow SMSF customers can generate the Notice of Intent and the acknowledgement letter instantly inside the Grow Portal. Full steps here: https://support.growsmsf.com.au/en/articles/11362342-completing-a-notice-of-intent-to-claim-form-via-the-grow-portal

Non-Grow SMSF customers will need to download and complete the form via the ATO website: Notice of intent to claim a deduction.

Critical Warning – Claim the Deduction

If you do not claim the tax deduction in your personal income tax return, the ATO automatically treats the contribution as a non-concessional contribution. This can trigger the bring-forward rule and create excess non-concessional contributions.

For example, as soon as you go even $1 over the current $120,000 (2025/26 year) non-concessional contribution cap, giving you $120,001 in contributions, you trigger the bring-forward rule, meaning for the subsequent two years you would only have $360,000 less $120,001 equals $239,999 cap space for the next two years, compared with up to $390,000 ($130,000 x 3) if you wanted to maximise contributions and trigger the bring-forward rule with the higher non-concessional caps from 1 July 2026.

Be careful!

Higher earners – Division 293 tax warning

Higher income earners should watch Division 293 tax. If your taxable income plus concessional contributions exceeds $250,000 in 2025-26, the ATO adds an extra 15% tax on the excess amount. This is on top of the normal 15% contributions tax inside the SMSF. A large catch-up contribution can push you into this bracket — always run the numbers first.

Learn more here: How Division 293 tax is calculated

Link to Contribution Reserving Strategy

Many SMSF trustees pair catch up concessional contributions with a contribution reserving strategy to smooth cash flow and manage contribution timing.

Read our full guide here: https://growsmsf.com.au/contribution-reserving-strategy/

Make Contributions Early – Beat the Deadline

The money must reach the SMSF bank account by 30 June 2026. Allow 2–3 business days for clearing, especially near EOFY.

30 June 2026 falls on a Tuesday, so this makes it a little easier this year.

Catch Up Concessional Contributions SMSF – Quick Checklist

- Confirm TSB was under $500,000 on 30 June 2025.

- Check myGov for unused caps.

- Use the Grow Portal for Notice of Intent (Grow SMSF customers only!).

- Claim the deduction in your 2025-26 tax return.

- Consider pairing with a contribution reserving strategy.

Catch up concessional contributions remain one of the strongest tax-planning tools for SMSF members. Act before 30 June 2026 and your SMSF (and your tax bill) will thank you.

Catch Up Concessional Contributions SMSF – FAQs

What are catch up concessional contributions? Catch up concessional contributions let you use unused portions of your concessional cap from the previous five financial years on top of the current year’s cap.

What is the concessional contributions cap for 2025-26? The cap is $30,000 for the year ending 30 June 2026. Eligible SMSF members can add unused caps from the last five years.

Who can use catch up concessional contributions SMSF? You must have had a total super balance below $500,000 on 30 June 2025. The rules apply to all super funds including SMSFs.

How do I check my unused catch up amount? Log into myGov → ATO services → Super → Information & Details → Carry-forward concessional contributions.

Can Grow SMSF members use the portal for paperwork? Yes. Grow customers can generate the Notice of Intent and acknowledgement letter instantly in the Grow Portal.

What happens if I forget to claim the tax deduction? The contribution is automatically treated as non-concessional. This can trigger the bring-forward rule and excess non-concessional contributions.

What is Division 293 tax? Higher earners pay an extra 15% tax (on top of the normal 15%) if taxable income plus concessional contributions exceed $250,000 in the year. A big catch-up contribution can trigger it.

When must the money reach the SMSF? By 30 June 2026. Transfer at least 2–3 business days early.

Will the cap increase next year? Yes. From 1 July 2026 the concessional cap rises to $32,500.

Do I need advice? Yes. Speak to your SMSF specialist or accountant before acting.