Segregated SMSF accounts can best be described as ‘sub-accounts’ within a self-managed super fund where each member has their own separate accounts and investments rather than having everything ‘pooled’ together with other members of the fund. Segregated accounts are uncommon because 93% of SMSFs have either one or two members and most with two members are couples so having all investments (and the subsequent returns on those investments) grouped together and shared is appropriate.

But what about the other 7% of SMSFs that have three or four members or situations where the members need or desire different investment strategies?

This is where segregated SMSF accounts can help.

Why segregate the SMSF accounts?

There are two main reasons members of an SMSF may want to separate their SMSF accounts and investments within the same fund:

- Tax purposes

- Investment strategies

Tax purposes

Where one member of an SMSF is retired and in pension phase and other members are still in accumulation phase using segregated SMSF accounts is one method of calculating ECPI. Exempt Current Pension Income is the percentage of income generated by the SMSF that is tax free.

There are some limitations segregating within an SMSF for tax purposes. Once any single member of the SMSF has a total superannuation balance of more than $1.6m the SMSF is not eligible to use the segregated method to determine the amount of income the SMSF can claim as tax free. However regardless of balances, an SMSF can still segregate for investment strategy purposes.

More on the segregated method to calculate ECPI from the ATO.

Many accountants mistakenly believe that when the 2017 changes came in limited the use of segregation for tax purposes, that you were no longer allowed to segregated an SMSF at all. This is untrue. You can still segregate the accounts for investment reporting and accounting purposes. The 2017 changes simply mean the segregated method can’t be used for tax purposes where one member has a total super balance above $1.6m. This is an integrity measure to ensure people with large SMSFs simply don’t switch investments around between taxable accumulation and tax free pension ‘pools’ depending on which assets have realised a capital gain that year.

Investment strategies

Segregating or separating an SMSF accounts and investments into different groups for different members of a fund can also be done for investment strategy reasons.

The most common example would be an SMSF where a member at or close to retirement would hold investments focused on capital stability and producing an income with low volatility, whereas a younger member with a long investment time frame would have more growth orientated investments. An SMSF where the members are a parent and adult child is an example.

Segregating SMSF accounts based on investment strategy is similar in some ways to how a large industry of retail super fund works. Younger members can elect for higher growth options, where older members can tap into more conservative, stable investments options to fund pension draw-downs.

How does SMSF investment segregation work?

Segregation of SMSF accounts is where each member (or a group of members) have separate and distinct accounts within an SMSF. This means:

- Their benefits are kept separate from other members within the SMSF;

- Each member has a separate bank account;

- Contributions and expenses (such as insurances) are not mixed with other members;

- Investments and their respective values, earning, income or losses are kept separate;

- At any point in time the value of each members benefit in the SMSF is the sum of their investments (less any taxes payable)

The following diagrams compare a standard pooled SMSF to a segregated SMSF.

Pooled SMSF accounts

Segregated SMSF accounts

As you can see when comparing pooled and segregated SMSF accounts, the SMSF has the same investments and accounts, however the difference comes down to whether those account are attached or allocated to the specific member.

Segregated SMSF accounts in practice

With the number of members allowed in an SMSF likely to increase from 4 to 6 members you may be looking at combining more people into an SMSF. There are a number of advantages and also some quite significant disadvantages to having more than you and your spouse / partner as members of your SMSF but something that can assist in providing more control is segregating the accounts.

Example of SMSF investment segregation

Let’s take the following example:

- 6 member super fund newly established 1 July;

- Each member adds $50,000 through either rollover of existing super or a non-concessional contribution;

- Each members has their own bank account and separate investment accounts;

- No additional contributions are made for each member during the year;

- No member expenses occur during the year (e.g. insurance premiums);

The 6 members of the SMSF implement separate investment strategies and invest in their chosen investments of Australian equities and US stocks with the following results (all in AUD):

Member 1 – Richie

Richie invests in a couple of mining stocks and an insurer (all ASX listed). Riche’s portfolio drops to $38,007 by 30 June.

Member 2 – Ellyse

Ellyse also invests into some ASX shares: CSL, Cochlear and Coles. Ellyse’s portfolio increases to $57,121 by 30 June.

Member 3 – Elon

Elon goes all in on TSLA stocks with his $50k. Elon’s portfolio spikes to $238,185 by 30 June.

Member 4 – Michael

Michael goes all in to SNAP stocks with his $50k. Michael’s portfolio increases to $84,000 by 30 June.

Member 5 – Scott

Scott invests in Nanosonics Limited with his $50k. Scott’s portfolio increases to $58,960 by 30 June.

Member 6 – Ash

Ash buys into AMP, Brickworks and BHP with her $50k. Ash’s portfolio drops to $44,960 by 30 June.

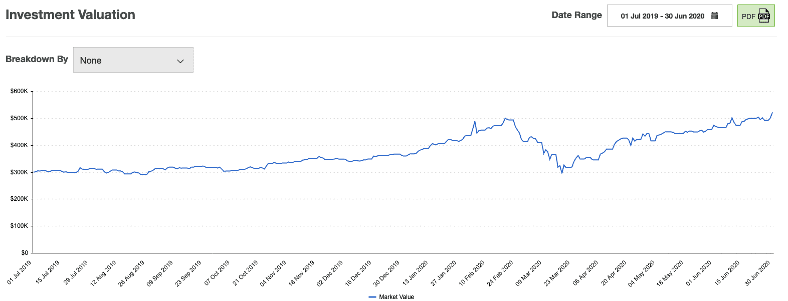

Overall the initial $300k SMSF balance increases to $521,263 by 30 June. This equates to an overall annual return for the SMSF of 73.75% – predominantly driven by Elon’s TSLA stocks. Not bad.

If the SMSF accounted for on a ‘pooled’ basis – which is how 99% of accountants would do it – each member balance would increase from $50,000 to $86,877. Even those who made loss-making investments would benefit from the overall rise in the SMSF value and the strong or very strong gains made by others.

What if the SMSF was segregated?

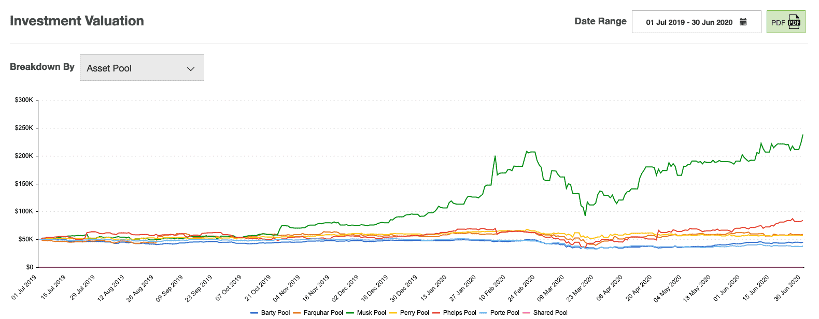

If the accountant or administrator of the fund set up segregated SMSF accounts, although the overall fund balance and returns for the year wouldn’t change, the individual balances of the members would be very different.

As you can see with the above comparison, when a segregated approach is used, each member gets allocated the profit or loss from their specific investments and accounts.

The follow chart shows the investment return for each individual member for the financial year to 30 June:

How to operate a segregated SMSF

Segregated SMSF accounts are more complex than a typical self-managed super fund are easy to get wrong.

Although each member of an SMSF (whether it’s 2, 4 or 6 members) can easily separate their investment accounts, there is some complexity in regards to how the taxation aspects are handled. The key reason is that although each member of the SMSF incurs their own tax liabilities (either from income, capital gains or contributions) as well their own tax credits (franking credits and foreign tax credits) the SMSF itself only lodges one tax return.

This means care must be taken to ensure each member pays their fair share of tax or receives their credits.

Take the example of a parent and adult child in the same fund. The retired parent earns tax free income and receives a refund of franking credits while the wealth accumulating child has a tax liability from income, gains and contributions. This means there is a need for the child to compensate the parent for the tax credits / franking credits they’ve absorbed for the year, i.e. there needs to be a transfer of cash between the child SMSF bank account and the parent SMSF bank account within the SMSF to compensate the parent for the reduce refund.

Similarly, tax losses including capital losses are at a fund level, meaning a member who makes a capital gain can effectively reduce their tax liability by using capital losses incurred by other members within the fund.

Ideally a segregated SMSF should be set up as segregated from day one. It is possible to change an SMSF from pooled to segregated, but it takes close co-ordination with a competent accountant to get the investment and bank accounts aligned to the members benefits as shown in the accounts at a particular date.

Fund level expenses

All SMSFs incur expenses which are at a ‘fund’ level rather than at a member level including:

- ATO SMSF levy ($259/year)

- ASIC annual registration fee for the trustee company ($55/year)

- Accounting, audit and administration fees

The members need to agree on how these expenses are paid as they fall due.

One method is to set up a separate ‘shared’ account which each individual member transfers their share of expenses into and all fund-level expenses are paid from this account.

Summary

Segregated SMSF accounts are useful when:

- Members of the SMSF are not a couple;

- Members are of different generations with different investments needs;

- The assets of the SMSF can be split and separated easy (i.e. not a lump asset like property);

- There is a desire to share costs across multiple parties

This article does not touch on who should be a member of your SMSF. That’s a topic for another day!

If you have any questions or would like to know more about whether a segregated SMSF may be useful for you, please get in touch.