A question we quite often asked by our clients is why they may have more than one pension account. In this article I will explore some of the reasons why having multiple pension accounts should actually be the norm, rather than the exception for SMSF clients.

Timing is everything:

One important thing to understand with superannuation pensions is that once they are started, they cannot be added to. This means that once a pension is started and a new pension account is created, you cannot make additional contributions to that pension account to increase it’s balance. You can however continue to make contributions to the SMSF, however these contributed amounts will sit in a separate accumulation or contribution account. Please note that this ‘separate account’ is not necessarily another bank account, but it is recorded as a different account on paper and forms part of your total member balance within the fund.

This most commonly occurs when you are undertaking what is known as a transition to retirement strategy (see below):

Transition to retirement strategies:

A transition to retirement strategy is where a person over the age of 55 has simultaneously commenced a pension from their superannuation fund, while still making contributions into an accumulation account. The thinking behind this strategy is that the additional employer or self-employed tax deductible concessional contributions are only taxed at 15%, rather than the individuals marginal tax rate – creating an overall tax saving.

Other advantages include the application of a 15% tax offset on ‘taxable’ amounts withdrawn as pension payments (where the person is under age 60) and also the fact that a tax exemption applies on any income or capital gains within the superannuation fund for assets that are used to support the pension payments. Where a person is over age 60 the impact is even greater as any pension amounts taken are not reported as taxable income.

This strategy unfortunately has lost some appeal for the current 2013 tax year due to the significant reduction in the concessional (tax deductible) contribution cap to $25,000 for all persons regardless of age and super balance.

So – what happens when you have started drawing a pension and then make additional contributions to your SMSF?

All contributions that you make will always go into your accumulation account within the SMSF. From there you can make a decision on whether on not to start a pension with the amounts contributed. For example, if the amount was a large non-concessional (personal) contribution from the sale of a property or an inheritance, it would make sense to commence a new pension with that amount immediately once the contribution has been made. This would ensure any income and capital gains within the fund relating to that pension would be tax free.

By contrast, if the contributions where received as small amounts throughout the year, for example from an employer or business, then it would make sense to wait until the start of the next financial to commence a new pension with the total of the contributed amounts and any associated income that is allocated.

***TIP*** When making contributions to your SMSF where you plan to use the amounts to start a new pension, it is suggested that wherever possible make single, large deposits or transfers all on the same day rather than over a number of days. The reason for this will be explained below.

Taking pension payments:

For a pension to be considered a pension, and for the SMSF to maintain the tax exemption that applies to the income and capital gains supporting the pension, the member must take at least one payment between the commencement date of the pension (if the pension started during the year) or the start of the financial year and 30 June (the end of the financial year). The amounts taken must also above the calculated minimum and below the maximum (where a maximum is applicable).

The only exception to this is when a pension is commenced in the month of June. When this occurs no pension is required to taken before 30 June.

Timing of when the pension payments are taken is extremely important to ensure that the pension minimum is met for the particular financial year. This can be illustrated with an example:

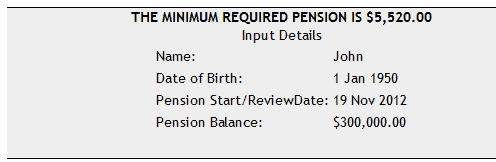

- We have John who is 62 and drawing a pension from his SMSF. John is the only member of his SMSF and 100% of his member balance is an account based pension. His minimum pension for the 2013 year is $12,000.

- John receives an inheritance and decides to make a non-concessional contribution to his fund of $300,000 on the 19th of November 2012

- John immediately commences a pension with the $300,000, and the additional amount that MUST be paid from that pension is calculated as follows:

This means that John needs to draw a total of $17,520 for the 2013 financial year to ensure he meets the minimum draw down requirements ($12,000 + $5,520).

Timing is everything in this example. In addition to having to draw out $17,520 in total during the 2013 financial year, at least $5,520 must be paid out to John between 19 November 2012 and 30 June 2013.

***TIP*** When you make large contributions to your SMSF during the year and are going to start a new pension, contact us to determine your minimum pension requirements so you can plan in advance how much you need to take and when you have to take it.

Separation of taxable and tax free components

Superannuation pensions have an interesting quirk about them: When a pension is commenced, the taxable and tax free components that make up the pension remain fixed in those proportions for the entire life of that pension. The tax free component is made up of personal non-concessional contributions,Small Business CGT amounts and Government co-contributions. The taxable component is basically everything else (namely concessional / tax deductible contribution and any earnings). These components can be found on your annual member statements.

When a pension is started, it will pick up the same taxable and tax free components in proportion based on the what those proportions are in the accumulation account – you cannot pick and choose different components for your pension – most of the time.

There are a couple of reasons why you would want to be able to split up the different components:

- When you are less then 60

- Estate planning

Pensions when you are under age 60:

When you are under age 60 and draw a pension (you need to be at least 55), the taxable proportion of your pension is still reported as taxable income in your personal income tax return (albeit with a 15% tax offset), however the tax free component does not have to be reported as taxable income.

This means that for someone under the age of 60, they want as much tax free component (and resulting tax free income) in their pension as possible.

If we take John from our example above and assumed he was aged 55 and he wanted to take $40,000 per year in pension income, we would take the bare minimum from his $400,000 pension balance (assuming it is mostly taxable) and the majority from his $300,000 pension that was started from non-concessional contributions and is entirely made up of the tax-free component.

Estate planning:

Once you are over age 60 life should be great – any pension you draw from your fund does not have to be reported on your personal tax return and the income within your SMSF that supports your pension is tax exempt. They say the only things certain in life are death and taxes. If you have set up your affairs correctly you may have escaped the taxes (for the moment at least) – but the death part is a little trickier.

When you pass away, any benefits paid to a dependant (as defined under taxation law) such as your spouse will be passed on free to tax. However, the taxable component when paid to non-dependants (such as adult children) tax will be paid by the SMSF at a rate of 16.5%. This has no impact on you, however your beneficiaries will lose a significant portion of their benefit. We regularly see clients where this ‘death tax’ on super can be hundreds of thousands of dollars.

There is however a couple of things you can do to reduce the potential tax burden:

- Re-contribution strategies

- Drawing more from a pension with a high taxable component and less from a pension with a high tax-free component

The re-contribution strategy is primarily used when you are between the age of 60 and 65 and have permanently retired. The strategy requires you to draw large tax free lump sum payments from your SMSF, then re-contribute large personal (non-concessional) contributions back into the SMSF and commence a new pension with those amounts. Although this strategy may seem simple, there are many more complexities, and it is important that the non-concessional contribution caps are not breached. Do not attempt such a strategy without the oversight of a SMSF specialist.

When you have multiple pension accounts, reducing the overall taxable component is basically a matter of taking the maximum you can from the pension with the high taxable balance, and only taking the absolute minimum from the pension with the high tax free component balance.

The management of this is purely and administration function and by default Grow SMSF staff will always apply the pension drawings on this basis – something that the majority of non-specialist accountants simply do not do.

Another strategy from an estate planning perspective is to build a detailed SMSF estate plan which directs the various superannuation pensions to the most appropriate recipient – for example a pension with a high taxable component could be transferred tax free to a spouse (via a reversionary pension) and a pension with a high tax free component could be paid to adult children with no additional tax to pay by the SMSF.

Separation of preservation components

The preservation of superannuation benefits determines when and how much can be taken from superannuation – either as a lump sum or pension. Benefits will typically be either preserved (i.e. cannot be accessed) or unrestricted non-preserved (can be freely accessed).

When a pension is commenced and you start drawing monies from your SMSF, firstly the unrestricted non-preserved amount must be taken. When a transition to retirement pension is commenced, there is an annual maximum limit of 10% of the member balance (including preserved amounts) that can be taken in the financial year, so another reason we would create multiple pensions is to preserve as much of the unrestricted non-preserved component as possible giving someone with a TRIS pension the ability to withdrawal more than the 10% which is typically available.

Summary

The subject of SMSF pensions is definitely complex, however if structured correctly will not only provide you an extremely tax effective income stream in your retirement, but can provide a benefit to your family without the tax man getting his (or her) hands on a cent.

Please note the information contained within this article is general information only and should not be considered advice. If you have any questions or would like to speak to one of our SMSF specialist advisers, please contact us.

Related Article: Re-Contribution Strategy “Magic Window” Created with Changes to Work Test and Bring-Forward Rules

13 comments

Heide Robson

July 1, 2017 at 2:54 pm

Great article. Printed it out and read every word. Kris, would be awesome if you could update the examples one day, but still a very helpful article. Thank you for writing it.

Neil Jones

January 14, 2022 at 11:48 am

In this post above you mention:

***TIP*** When making contributions to your SMSF where you plan to use the amounts to start a new pension, it is suggested that wherever possible make single, large deposits or transfers all on the same day rather than over a number of days. The reason for this will be explained below.

Not sure this was explained. Please confirm.

Kris Kitto

January 14, 2022 at 12:03 pm

The key reason it that allows for a deposit into an accumulation account to go in, then immediately be swept out same day (in the accounting records) into a new pension account, which ensures no taxable profit amount is allocated to a pension account that you’re attempting to keep 100% tax free component (e.g. if doing a re-contribution strategy).

More information in this article: https://growsmsf.com.au/re-contribution-strategy-magic-window-created-with-bring-forward-rule-change/

Or, just follow the instructions of a competent SMSF accountant/advisor!

Garry Luscombe

June 16, 2023 at 1:37 pm

Can I merge 2 pension accounts sitting within the same SMSF?

Kris Kitto

June 16, 2023 at 1:54 pm

Technically yes. It’s better described as commuting (stopping) two pensions with the proceeds going back into accumulation, then immediately creating a new combined pension.

TBAR reporting required and of course it will merge the taxable and tax free components of the pensions.

Running multiple account-based pensions is very common. The goal should be to preserve the tax free component pensions for estate planning and eat up the pensions with high taxable component.

Bill Nagle

March 4, 2024 at 11:09 am

Thanks Kris, when commuting multiple pensions back into an accumulation account how are the tax free and taxable components recalculated and by whom? Is it a weighted average ( I have 6 in my smsf, all with different proportions) and is it done by the ATO through the TBAR reporting process? I am closing my SMSF and rolling the funds into a mainstream super fund. Bill

Kris Kitto

March 4, 2024 at 11:16 am

It’s all worked out by the SMSF accountant.

Basically everything gets stacked together back in the accumulation account, so the total taxable and tax free components of the all the pensions will equal the total taxable and tax free of the accumulation account. Any earnings allocated while it’s in accumulation will be added to the taxable component.

You must ensure the minimum pension (pro-rata) is taken from the pensions before they’re commuted to ensure the tax exemption applies prior to closing the pension accounts. If you have any pensions with high tax free component, maybe think about keeping these quarantined and potentially rolled into a different super pension account rather than combining everything into a single accumulation account.

None of the above can be considered personal financial advice as I don’t know you or have any information about you. The above is purely factual information. For advice specific to your circumstances please see a licensed financial adviser.

James Molesworth

May 26, 2024 at 10:33 pm

Hi Kris,

Thank you for the information. Very helpful.

I have a procedural question about rollovers out of a multiple pension SMSF.

I have two account-based pensions in my SMSF. The first one has a high taxable component. The second one was created with a maximum three year recontribution strategy (non concessional) and so has a taxable component of nil.

I now want to do a PARTIAL rollover from the SMSF to a retail fund, as preparation to closing down the SMSF, then start a new pension in the retail fund to keep the high taxable bit isolated… so I can hit it with a future re-contribution cycle. So I want to rollover just from the account-based pension with the high taxable component, exactly for the estate planning reasons, as you described above.

The silly-souding question is this: How do I nominate which account based pension to perform the rollover from?

None of the sample rollover request forms from the ATO or Retail funds that I have seen nominate a specific FROM pension account number. They just have the member number.

Do I just textually specify this in a rollover request letter to the SMSF Trustees?

Thanks and regards,

James.

Kris Kitto

May 27, 2024 at 8:45 am

The following is general information and cannot be considered personal financial advice.

A pension interest in an SMSF cannot be rolled over to another fund. Only accumulation accounts can be rolled over to a different superannuation fund.

If a person has multiple pensions in their SMSF, they need to instruction their SMSF administrator/accountant to commute the selected pension to accumulation and then instruct them to commence the rollover process to an external fund of their choice.

Shenaaz

May 27, 2024 at 11:05 am

I commenced a Pension in April 2017 with less than the transfer balanced cap. I have some money in an accumulation account, is it better to to stop my existing pension and re-start it with the new balance, or keep my existing pension going and start a second pension account?

Kris Kitto

May 27, 2024 at 11:14 am

That’s very specific personal financial advice your seeking.

Best to seek advice from a licensed financial adviser.

Rob

October 6, 2024 at 10:56 pm

Kris , I we have an industry super in pension phase and SMSF with investment property in pension phase, do you need to meet minimum drawdown for each of the super individually or on the whole? In other words, if I am not able to meet the minimum drawdown in a particular from SMSF , then can i draw higher % from industry super in that year so that overall minimum drawdown is met?

Kris Kitto

October 8, 2024 at 8:03 am

No.

Each pension account, e.g. SMSF + industry super, has it’s own minimum draw down requirement.

You must draw the require % minimum from each pension individually.

Drawing extra from one account has nothing to do with the other.