If you have typed “SMSF” into Google while researching SMSFs and been bombarded with adverts for esuperfund, you are not alone. They are one of the most heavily promoted SMSF providers in Australia. This esuperfund review article gives you a straight, honest comparison of esuperfund vs Grow SMSF for 2026: how each business model works, what fees you will actually pay, where any hidden costs sit, and which provider suits which type of trustee.

I am Kris Kitto, Director of Grow SMSF. I have looked after thousands of SMSF clients for over 20 years and have written about esuperfund multiple times since 2015. Over that time, my perspective on the esuperfund business has changed. As a fellow SMSF business owner, I have a large amount of respect for the esuperfund business. Esuperfund has made a significant contribution to the SMSF space (industry?) by making SMSFs accessible to tens of thousands of Australians who may not have otherwise started an SMSF due to perceived complexity and high costs. I would be surprised if there we any accountants or financial advisers in the country who don’t have an SMSF client that originally started with esuperfund.

I have updated this esuperfund review for 2026 to reflect esuperfund’s current fee structure, their “pay nothing until 2028” promotion, and a significantly changed competitive landscape.

Short answer: esuperfund suits a specific niche of trustees who want a fully DIY, low-touch, single-market SMSF and are comfortable with no phone support. For anyone who values flexibility, direct human access, or plans to hold property, use advanced solutions Interactive Brokers, or build a complex strategy — Grow SMSF is the stronger choice.

Navigate to Key Sections

How esuperfund makes money — understanding the business model

Before comparing fees, it is worth understanding how esuperfund generates revenue. This is not a criticism — it is simply important context for any trustee evaluating the real cost of using their service.

esuperfund operates a hybrid model. They charge an annual fixed fee ($1,499 per year from the 2027 financial year onwards) and — as disclosed in their Financial Services Guide — receive commissions on products their clients may use. These include:

- Share trades via ebroking (CMC white-label): Up to $16.23 per trade (under $30,000) or up to 0.073% per trade (over $30,000)

- CMC Markets: Up to 50% of the brokerage rates changes by CMC Markets for share trades.

- ANZ V2 Plus bank account: Up to 0.55% per annum on the cash balance held

- Insurance premiums (Zurich): Up to 20% per annum of the insurance premium

- Insurance premiums (AIA): Up to 30% per annum of the insurance premium

- ING Direct bank account: Up to 0.20% per annum on the cash balance

- AMP Term Deposits: Up to 0.20% per annum on the deposit balance

All of this is disclosed in their FSG, as required by law. The important point is this: when esuperfund steers you toward their default bank account or their ebroking platform, there is a commercial reason beyond convenience. As a customer, you don’t necessarily pay more than what you would going direct — but the products available through esuperfund’s default stack are not always the lowest-cost options available to SMSF trustees in 2026.

It is important to note it is not mandatory to use any of the above listed products with esuperfund. However, by using different products, it is likely to significantly change the level of work involved. More on this later.

Grow SMSF earns no commissions, rebates, or referral fees from any bank, broker, or investment provider. You pay a fee; we provide the service. There is nothing else.

The “free setup” and “pay nothing until 2028” — what it actually means

The free setup

esuperfund advertises free SMSF setup. This is accurate — but only for individual trustee structures. If you want a corporate trustee (a special purpose company), there is an additional fee to establish the company. Based on their current pricing, this is $899 — bringing the real setup cost to around $899 for a corporate trustee setup with esuperfund.

Grow SMSF charges $880 for individual trustees and $1,520 for a corporate trustee (which includes the current $611 ASIC registration fee for a special purpose company). The gap between esuperfund and Grow for a corporate trustee setup is approximately $596.

That $596 difference buys you:

- A guided setup process with a real humans available by phone

- Full service experience doing everything required to get your new SMSF up and running as quickly and smoothly as possible

- Access to Grow’s preferred brokers (IBKR, Selfwealth, Betashares Direct)

- A dedicated senior SMSF Account Manager from day one

- No requirement to categorise and code your own transactions

- Phone support for all SMSF related items

For most trustees, a corporate trustee is the right structure. The ATO, SMSF specialists, and virtually every legal practitioner in the field recommend a corporate trustee for all but the simplest two-member arrangements. The “free setup” with esuperfund is free only if you choose the structure most professionals recommend against.

Most people will only set up an SMSF once in their lives. For this reason it makes sense to do it correctly and obtain professional support throughout. That’s where Grow SMSF excels.

Free first year and “pay nothing until 2028”

esuperfund’s current promotion for new SMSFs reads: the 2027 financial year annual fee is free. If you set up now, your SMSF’s first financial year will be the year ending 30 June 2027 — so you pay nothing for that year’s compliance work.

The next (first) fee — for the 2027/28 financial year’s work — is charged in January 2028. So you’re effectively paying the 2027/28 year fee in advance, considering the actual work will be completed some time between July 2028 and May 2029. Then subsequent fees are charged each January. Depending on when esuperfund completes your work (which also depends on when you complete the work you need to do) you may have paid two years worth of fees by the time they complete and lodge the 2027/28 year (e.g. if completed in February to May 2029).

The “pay nothing until 2028” framing comes from this: if you apply now, esuperfund says the SMSF commencement date will be 1 July 2026, the first financial year will end 30 June 2027, and the ESUPERFUND annual fee for that 2027 financial year is free. The next esuperfund annual fee, for the 2028 financial year, is payable in January 2028.

This is clever marketing. It genuinely reduces upfront friction and makes an SMSF feel more accessible to people who might otherwise hesitate at fees. However, the “free” offer is conditional: it applies only if the SMSF setup and activation proceed, and it does not remove other possible costs such as the ATO supervisory levy, company trustee setup costs where applicable, investment fees, or later annual fees.

Another interesting aspect is esuperfund collects all their annual fees mid-January each year. Their website says they have over 35,000 SMSFs using their platform. If 90% of their customer base is outside of their ‘free’ first year, that means esuperfund would be banking over $47 million in customer monies each January. That’s money they’re using to earn interest and fund their operations. Similar in some ways to how Starbucks uses customer gift cards and loyalty programs to fund its expansion. Again, clever business practice.

Is the same deferral available with Grow? Yes. Grow charges annual fees in arrears — after the compliance work is completed. For a fund set up in July 2026, Grow’s first annual fee would also typically land in late 2027 or early 2028, depending on lodgement scheduling. If you want to maximise the deferral at Grow, simply request a late lodgement date (28 February 2028 deadline).

The following example compares the timing of fees for esuperfund and Grow:

| Item | esuperfund | Grow SMSF |

|---|---|---|

| Date of New SMSF Setup | July 2026 | July 2026 |

| Setup Fee (corporate trustee) | $899 | $1,520 |

| First Return | 2026/27 | 2026/27 |

| Due Date of First Return | 28 February 2028 | 28 February 2028 |

| First Annual Fee | $1,499 | from $1,485 |

| Date of First Annual Fee | 15 January 2028 | Upon completion of 2026/27 As late as February 2028 |

*All fees current as of the date of publication and are subject to change. The esuperfund first annual fee in January 2028 is a pre-payment of the fee for the 2027/28 year for work to be completed sometime between July 2028 and May 2029.

The real cost of esuperfund vs Grow SMSF — a 2026 comparison

Annual fee trajectory: 2016 to 2026

In 2016, esuperfund charged $799 per year. Their current annual fee is $1,499 — an increase of $700, or approximately 87% over 10 years. On a compounded basis, that is roughly 6.5–7% annual fee growth. Australian CPI over the same period averaged approximately 3.1% per year.

esuperfund is still perceived by many as the “cheap option.” The gap has narrowed enormously in recent years. Their $1,499 annual fee is now above Grow’s entry-level Starter plan at $1,485 per year.

| Item | esuperfund | Grow SMSF | Notes |

|---|---|---|---|

| Setup (individual trustees) | Free* | $880 | esuperfund free for individual trustees only |

| Setup (corporate trustee) | $899 | $1,520 | Grow includes ASIC $611 registration fee. Gap is ~$596. |

| Annual fee (standard) | $1,499 | $1,485 (Starter) | Grow Starter now cheaper than esuperfund standard rate |

| Annual fee (property/LRBA) | $1,499 (no extra) | $2,255 (Property Base) | Grow property tier includes annual valuations (residential) and title searches. esuperfund does not include annual property valuations or title searches. |

| Broker lock-in | ebroking (CMC) default; other brokers require manual data entry by you | Any broker — IBKR, Selfwealth, Betashares Direct, others – all data fed | Grow has direct data feeds to 20+ brokers and 50+ banks |

| ATO Supervisory Levy | $259/yr ($518 yr 1) | $259/yr ($518 yr 1) | Paid to ATO — same for both |

| ASIC annual review (corporate trustee) | $70 | $70 | Paid to ASIC — same for both |

| Wind-up fee | $699 | $550 – $1100 | Additional fee to close the SMSF |

*esuperfund “free setup” applies to individual trustee structures only. Corporate trustee setup incurs an additional company establishment fee. Verify current esuperfund pricing at esuperfund.com.au/fees. Grow SMSF fees effective 2025–26. See full Grow SMSF fee schedule. Fees accurate as of the date of publication, but subject to change.

The hidden cost: brokerage and FX fees

This is where the headline annual fee comparison breaks down quickly.

esuperfund’s default broker is ebroking. Brokerage on ASX trades via ebroking costs $15.23 minimum (under $30,000) — and esuperfund receives a commission on those trades as disclosed in their FSG.

Grow’s preferred brokers for ASX investing include Selfwealth ($9.50 flat per trade, data fed, CHESS) and Betashares Direct ($0 brokerage ASX, custodial).

For an SMSF trustee making 20 ASX trades (less than $25k per trade) per year:

| Item | ebroing (esuperfund) | Selfwealth (Grow) | Betashares Direct (Grow) | Annual savings |

|---|---|---|---|---|

| Brokerage per trade (ASX <$25k) | $29.95 minimum | $9.50 flat | $0 | $20.45 to $29.95 per trade |

| 20 trades per year | $599 | $190 | $0 | $409 to $599 |

| Annual admin fee | $1,499 | $1,485 | $1,485 | $14.00 |

| Total annual cost (20 trades) | $2,098 | $1,675 | $1,485.00 | Up to $613 cheaper with Grow |

Ebroking pricing can be found here.

For US stock investing via Interactive Brokers through Grow, the FX cost differential is even more significant — 0.03% vs CMC’s 0.60%. You can find an excellent comparison between brokerage platforms via Passive Investing Australia here.

Esuperfund does not have IBKR integration at all. If you want global markets with IBKR-level pricing, esuperfund is not the right solution. See our full IBKR SMSF solution.

The technology: esuperfund’s proprietary platform

One area where esuperfund deserves genuine credit: they built and maintain their own SMSF accounting platform. Almost every other SMSF administrator in Australia — including Grow — uses third-party software such as Class Super, BGL 360, or SuperMate. These are excellent platforms but carry unavoidable monthly licence fees for the SMSF business.

By running a proprietary system, albeit with all the technology and maintenance costs that come with it, esuperfund can spread that cost across their entire client base. When you have tens of thousands of SMSFs on one platform (esuperfund discloses 35,000 SMSFs), the per-client cost is minimal, and it contributes to their ability to price at $1,499.

The tradeoff: their proprietary system may have less functionality or fewer integration points than industry-standard platforms. Grow uses Class Super — widely regarded as the most comprehensive SMSF accounting platform in Australia — which integrates with every major bank, broker, and investment platform via direct data feeds.

You are the accountant with esuperfund

This is perhaps the clearest structural difference between the two services, and it is worth being direct about it.

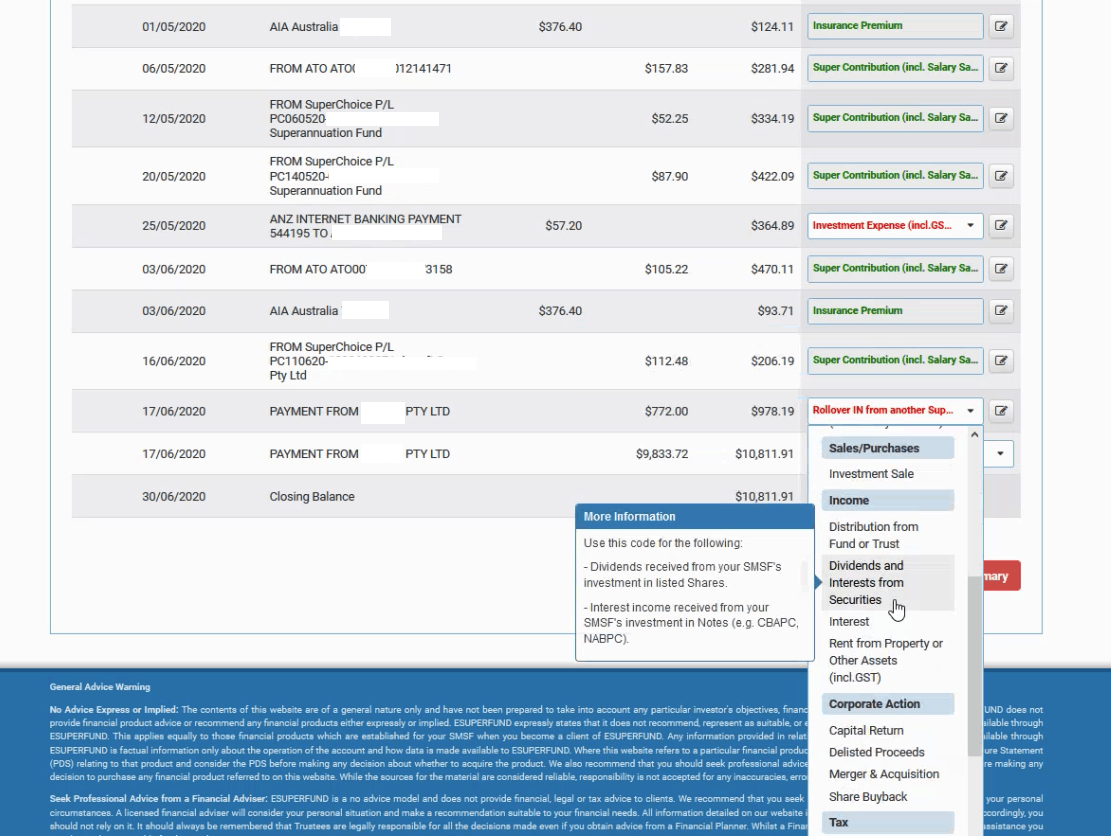

With esuperfund, their client portal requires you to:

- Complete a detailed annual checklist for your fund

- Categorise and code transactions in their system

- Upload supporting documents for the auditor

- Provide data manually for any bank or broker outside esuperfund’s default stack

- Interpret and action system notifications without phone support

Some trustees genuinely enjoy this. esuperfund has built an excellent library of educational content, and many of their clients engage deeply with the DIY aspect of managing their SMSF. If you are that type of trustee — data-driven, self-sufficient, and holding a simple share portfolio — esuperfund can work well.

Grow’s view is that trustee time is better spent on investment research and strategy, not bookkeeping. That is what you pay Grow for. Our clients’ ongoing compliance obligations are handled with minimal effort from them, because we invest heavily in automation and direct data connections. Their time is spent on their portfolio — not chasing paperwork.

Another way to think about it: esuperfund provides an online accounting platform for your SMSF, with an added tax lodgement and independent audit function. By comparison, Grow is a full service provider. We do all the accounting and administrative aspects for your SMSF. You simply invest your super on your terms and pay fees as required.

Service and support: the biggest practical difference

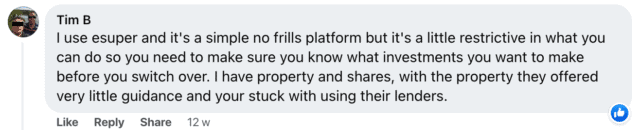

Try to find esuperfund’s phone number on their website. Take as long as you need. You will not find one, because it does not exist.

All esuperfund client communication occurs through their online portal — messages, queries, and responses. For simple, routine matters this is often fine. For complex situations — a property purchase that needs urgent direction, a compliance question before signing a contract, a pension commutation that needs to be handled correctly — the absence of a human voice can be costly.

Some esuperfund clients have no problems with this model. Others tell us, when they eventually call Grow, that they spent weeks going back and forth on a matter that would have taken two minutes on the phone to resolve.

Three real examples from our practice (details changed):

- A trustee invested in a private unit trust. The esuperfund auditor issued an Auditor Contravention Report to the ATO because the trustee could not get guidance on what documentation was required. A 10-minute phone call would have resolved it. The ATO compliance action took months to clear.

- A mother and son SMSF with a pension member inadvertently over-drew the pension balance because she received incomplete guidance from the portal (or misinterpreted correct information) about her allowable drawdown amount. A serious breach resulted.

- A doctor set up an LRBA property purchase through esuperfund, signed the purchase contract in the wrong name (his personal name, not the bare trustee), and could not get real-time guidance. The fund effectively made an illegal loan to a member. The only solution was to sell the property.

These are not isolated edge cases. They are the type of errors that happen when people are dealing with complex, high-stakes financial decisions without access to a specialist they can call.

Grow clients have access to:

- A dedicated senior SMSF Account Manager — an SMSF Specialist Advisor with 10+ years of experience

- A phone number that is answered by a human during business hours: 1300 651 263

- Growbot — our AI agent that handles many routine queries instantly, 24/7

- A team of SMSF accountants and administrators who know you and your fund

esuperfund vs Grow SMSF: side-by-side comparison

| Feature | esuperfund | Grow SMSF |

|---|---|---|

| Annual fee (standard) | $1,499 | From $1,485 (Starter) |

| Setup fee (corporate trustee) | ~$899 | $1,520 |

| Phone support | No phone number | Yes — 1300 651 263, business hours |

| Dedicated account manager | No | Yes — senior SMSF accountant |

| AI support agent | No | Yes — Growbot, 24/7 |

| Trustee does own transaction coding | Yes — required | No — Grow handles this |

| Broker flexibility | ebroking default; others require manual data entry | Any broker — 20+ direct data feeds |

| Interactive Brokers (IBKR) support | No | Yes — full IBKR SMSF integration |

| Cryptocurrency support | Yes – but limited | Yes — Swyftx, other exchanges, self-custody |

| Property / LRBA support | Available, no extra fee | Deep expertise, valuations and title searches included in property tier |

| Accounting platform | Proprietary (in-house) | Class Super (industry leader) |

| Broker commissions earned by provider | Yes — disclosed in FSG | No — fee for service only |

| Transfer an existing SMSF allowable | No | Yes. Free — dedicated transition process |

Who should use esuperfund

- You want a fully DIY approach and enjoy the hands-on administration work

- Your SMSF holds only ASX shares or ETFs via ebroking, with no plans for property, crypto, or US/international trading via a platform like IBKR

- You are comfortable with portal-only support and no phone access

- Your fund is straightforward and unlikely to encounter complex compliance questions

- The lower headline annual fee is your primary decision criterion

Who should use Grow SMSF

- You want a real person you can call when something important comes up

- You are planning or already hold property in your SMSF (or are considering it)

- You want access to Interactive Brokers for global markets at institutional FX rates

- You hold cryptocurrency or are considering it (including support for self-custody)

- You do not want to categorise your own transactions or upload your own documents

- You are currently with esuperfund and have outgrown what they can offer

- You want transparent, fee-for-service pricing with no broker commissions in the background

Switching from esuperfund to Grow: how it works

This is one of the most common transitions we handle. Here is what it looks like in practice:

- No cost to transfer to Grow — there is no transfer or onboarding fee from our side

- Grow has a streamlined process for transferring from esuperfund — no heavy lifting required from you

- If esuperfund has debited your account for a year’s fees but has not yet completed the work, they will refund the difference upon your departure

- We support the ANZ V2 Plus account (esuperfund’s default), so if you already have one, it is often just a form to give Grow read access to your transaction data

- If you have lodgements outstanding or are behind with the ATO, we can handle multiple years of catch-up work — this is common and we see it regularly

The esuperfund exit fee of $1,499 only applies if you have not yet paid at least one year’s annual compliance fee. Most trustees who are ready to switch have paid at least one year — in which case there is no exit fee from esuperfund’s side either.

Ready to talk?

If you are currently with esuperfund and wondering whether Grow is a better fit — or if you are comparing providers before setting up — the fastest way to get a clear answer is a 15-minute call.

Call us directly: 1300 651 263 — we answer during business hours. That’s something you cannot do with esuperfund.

Or book a call with Garry Johnston, who oversees the team that specialises in esuperfund transitions: Book a free consultation

Already ready to start the transfer? Commence your SMSF transfer here →

FAQ

Is esuperfund cheaper than Grow SMSF in 2026?

Not necessarily. esuperfund’s standard annual fee of $1,499 is now above Grow’s Starter plan at $1,485. Once you factor in brokerage costs on ebroking vs Selfwealth or Betashares Direct, many trustees actually pay less in total with Grow. The “free setup” only applies to individual trustee structures — not the corporate trustee structure that most practitioners recommend.

Does esuperfund have a phone number?

No. esuperfund does not publish or operate a client phone number. All communication is through their online portal. Grow’s number is 1300 651 263 and is answered by a human during business hours.

What is the esuperfund “pay nothing until 2028” promotion?

If you set up a new SMSF with esuperfund now, the first financial year’s compliance fee (for the year ending 30 June 2027) is free. The next fee is charged in January 2028 for the 2027–28 year’s work. Grow can provide similar timing for the first year fee if this is a deal breaker for your new SMSF.

Can I use Interactive Brokers (IBKR) with esuperfund?

No. esuperfund does not have an IBKR integration. If you use IBKR as your broker with esuperfund, you would need to manually provide transaction data. Grow has a dedicated IBKR SMSF solution with full platform access and automated compliance.

Is it easy to switch from esuperfund to Grow?

Yes. Grow has a dedicated transition process for esuperfund clients. There is no transfer fee from Grow’s side. If esuperfund has already debited fees for uncompleted work, they will refund the payment.

Does esuperfund support cryptocurrency in an SMSF?

esuperfund offers limited crypto support through specific integrations. Grow has deep integration with Swyftx, supports other Australian crypto exchanges, and has experience with self-custody SMSF structures for Bitcoin and other digital assets.

Does esuperfund support SMSF property and LRBA?

esuperfund does offer property and LRBA support with no additional annual fee. However, they do not provide specialist guidance by phone during the purchase process — which is when most costly mistakes occur. Grow’s property tier includes annual valuations, title searches, and a dedicated senior specialist you can call at any point during the purchase.

How has esuperfund’s annual fee changed over time?

In 2016 esuperfund charged $799 per year. Their current rate is $1,499 — an increase of approximately 87% over 10 years, well above CPI growth of approximately 3.1% per year over the same period. The gap between esuperfund and Grow has narrowed significantly.

How does esuperfund make money beyond the annual fee?

esuperfund discloses in their Financial Services Guide that they receive commissions on products their clients use, including share trades via ebroking (up to $15.23 per trade or 0.068%), the ANZ V2 Plus bank account balance (up to 0.60% per annum), and insurance premiums (up to 27.5% per annum for AIA). Grow earns no commissions from any third-party product or provider.

Thank you for reading our esuperfund review for 2026.